First Version: July 11, 2024—This Version: April 19, 2026

1 Introduction

Firm heterogeneity plays a central role in many economic questions. Seminal models of firm dynamics and firm size distributions, such as Lucas (1978), Hopenhayn (1992), and Melitz (2003), attribute firm heterogeneity primarily to differences in total factor productivity (TFP), assuming homogeneous returns to scale (RTS) across firms. Large and persistent TFP differences within industries have been extensively documented across countries and time periods (see Syverson (2011) for an overview), while little is known about RTS differences. In this paper, we allow for more general heterogeneity in production technologies by focusing on RTS heterogeneity. Using a broad set of estimation methods, we first examine empirically whether larger firms have technologies that are more productive (high TFP), more scalable (high RTS), or both. Second, we demonstrate the importance of this distinction by studying the efficiency costs of misallocation due to financial frictions—an issue central to a variety of quantitative questions.

In our benchmark approach, we estimate nonparametric production functions building on Gandhi, Navarro and Rivers (2020) (henceforth GNR), which recovers output elasticities of labor, capital, and intermediate inputs—thus, RTS—along with TFP at the firm-year level. Differences in local elasticities under a common non-homothetic production function are identified from variation in input expenditure shares and from the covariance between input and output levels, controlling for the endogeneity of inputs to TFP. We extend this method by embedding it within a clustering framework to disentangle ex-ante technology differences across firms from variation in local elasticities due to non-homotheticities.

In our main empirical analysis, we use administrative panel data for the universe of incorporated Canadian firms, accounting for over 90% of private business sector output from 2001 to 2019. This dataset provides detailed balance sheet information, including revenues and the total cost of labor, capital, and intermediate inputs. To validate our results, we replicate the analysis for manufacturing plants using U.S. census data as well as for eleven European countries using the Moody’s Orbis dataset.

We start by estimating production functions for each two-digit NAICS industry. Beyond the well-documented TFP heterogeneity, we uncover substantial RTS variation among firms within the same industry. The average within-industry difference between the \(90^{th}\) and \(10^{th}\) percentiles (P90–P10) of RTS is 8 percentage points (p.p.). Interpreted as deviations from constant returns to scale, these differences are large.1 By construction, heterogeneity in RTS reflects dispersion in output elasticities of inputs. The P90–P10 of elasticities is 0.36 for intermediates and labor versus 0.08 for capital. Output elasticities closely track input revenue shares.2

Our key finding is that RTS increases with firm revenue (and alternatively with employment or value added), especially above the median. Within industries, the largest 5% of firms have 8 p.p. higher average RTS than those in the bottom 50%. This pattern is driven entirely by higher output elasticities of intermediate inputs for larger firms. Labor and capital elasticities generally decline with firm size, albeit with some variation across samples and specifications.

Equally important, RTS heterogeneity is highly persistent: firm fixed effects explain 75% of the variation conditional on age and size, and an autocovariance analysis attributes just 11% to transitory shocks. To investigate whether this persistence primarily reflects genuine technological differences across firms or non-homothetic variation along a common production function, we embed the GNR method within an iterative clustering framework that allows firms to operate distinct production technologies within industries. This approach shows that 83% of the RTS–size gradient reflects ex-ante differences across technologies rather than within-technology variation along a common production function.

TFP increases with firm revenue only up to the 90th percentile, but then levels off and declines sharply among the largest firms.3 In contrast, RTS continues to rise—convexly—for the largest firms, indicating that their size advantage reflects greater scalability rather than higher productivity. Consistent with this pattern, a decomposition exercise shows that technological heterogeneity explains roughly two thirds of firm-size dispersion within industries, with the remainder explained by TFP differences.

Our GNR approach allows for adjustment frictions and market power for capital and labor inputs but not firm-specific markups or factor-biased productivity. To address these limitations, we apply Demirer (2025)’s method, which permits heterogeneous markups and factor-augmenting productivity shocks—at the cost of stronger assumptions on the labor input choice and the functional form of the technology. We find an even steeper RTS–size gradient, consistent with the view that physical RTS increases more strongly with firm size than revenue-based RTS, as expected if markups increase with firm revenue.4 As additional robustness checks, we also estimate specifications with homogeneous relative factor elasticities but heterogeneous RTS, which similarly produce a strong RTS–size gradient, and show that the gradient becomes even more pronounced when we include intangibles in measuring firms’ capital.

Our results are remarkably consistent across countries and data sources as well. While our baseline uses data for the Canadian economy, we find a similarly strong RTS–size gradient among U.S. manufacturing plants and across eleven European countries using firm-level Orbis data—the gradient is positive in every single one and of broadly similar magnitude.

We also revisit several well-known empirical patterns in firm heterogeneity commonly attributed to TFP differences. We find that RTS is a stronger predictor of firm growth and survival over the life cycle than TFP. High-wage firms also tend to have higher RTS. Linking firms to their owners, we show that wealthier households own firms with more scalable technologies. These secondary findings highlight the importance of incorporating realistic RTS heterogeneity for a variety of applications, including wage and wealth inequality.

To investigate the quantitative implications of our findings, we incorporate heterogeneous RTS into a standard incomplete markets model of entrepreneurship (e.g., Quadrini (2000); Cagetti and De Nardi (2006)).5 In the model, agents choose whether to supply stochastic efficiency units of labor or to operate a private business under a stochastic technology that depends not only on a standard idiosyncratic TFP term (\(z\)) but also on an idiosyncratic RTS term (\(\eta\)). Entrepreneurs must finance at least a fraction \(\lambda\) of their input expenditures using their own wealth. Our main exercise compares the effects of increasing the financial friction \(\lambda\) on output and productivity in two different economies: the conventional \(z\)-economy, where technological heterogeneity stems from TFP alone, and the \((\eta,z)\)-economy, which incorporates heterogeneity in both RTS and TFP based on our empirical estimates. We calibrate both economies to match key moments such as the firm-size distribution.

We find that in the \((\eta,z)\)-economy, financial frictions generate over twice the output losses compared to the \(z\)-economy. Static misallocation of inputs accounts for the bulk of output losses in both economies and is about twice as large in the \((\eta,z)\)-economy. To build intuition, we analytically show in a static endowment economy that a given wedge in marginal products leads to larger misallocation when constrained firms have relatively higher RTS—an endogenous feature of our dynamic model. Dynamic effects further exacerbate output losses in the \((\eta,z)\)-economy, due to under-accumulation of capital and distortions in the selection into entrepreneurship. Intuitively, a highly productive (high-\(z\)) but poor potential entrepreneur can operate profitably at a small scale, making it easier to grow despite the friction. In contrast, a highly scalable (high-\(\eta\)) but less immediately profitable business struggles to outgrow the friction, and the entrepreneur may never enter the market. These results highlight the critical importance of accounting for RTS heterogeneity for a broad set of quantitative questions related to misallocation, including capital taxation (e.g., Guvenen et al. (2023); Boar and Midrigan (2022); Gaillard and Wangner (2021)).

Literature Review. A growing literature documents RTS heterogeneity across industries and over time, studying its implications. Gao and Kehrig (2017) estimate substantial cross-industry variation in U.S. manufacturing and show that higher-RTS industries are more concentrated. Ruzic and Ho (2023) demonstrate that industry-level RTS heterogeneity is first-order for misallocation measurement. Smirnyagin (2023) shows that firms in high-RTS industries are disproportionately absent from recessionary cohorts due to financial frictions. At the aggregate level, Chiavari (2024) shows that the rise in average U.S. RTS since 1980 contributed to declining business dynamism. At the firm level, Mertens and Schoefer (2025) contemporaneously document that growing firms shift their input mix from labor toward intermediates—consistent with our findings—while Demirer (2025), in work focused on markup measurement, notes RTS heterogeneity across countries and firms. Clymo and Rozsypal (2025) study firm cyclicality across age and size groups and argue that heterogeneous RTS help explain why larger firms are more cyclical. Our paper contributes to this literature by establishing, across countries, datasets, and estimation methods using comprehensive administrative firm data, that differences in RTS between firms are at least as important as differences in TFP for firm-size dispersion within industries—and increasingly so among the largest firms. We further show that the RTS–size gradient primarily reflects persistent differences in production technologies across firms rather than within-technology variation along a common production function.

Several papers study specific microfoundations for the size-RTS relationship. Lashkari et al. (2024) show that the nonrival nature of IT capital generates higher RTS for IT-intensive firms and accounts for a significant share of rising concentration in France. Hsieh and Rossi-Hansberg (2023) emphasize ICT-enabled, fixed-cost-intensive technologies that allow top service firms to replicate production across locations, generating firm-level scale economies. Argente et al. (2024) show that firms with more scalable, standardized expertise face flatter marginal cost curves and grow larger. Chen et al. (2023) study size-dependent scale elasticities arising from non-homothetic managerial inputs. In each of these models, firm-level scalability arises endogenously with size through a single channel rather than being an independent, persistent firm characteristic. In contrast, we measure the full extent of RTS heterogeneity across firms—capturing variation from all sources, including ex-ante technology differences—and show through a quantitative model that it more than doubles the efficiency costs of financial frictions relative to a conventional TFP-only calibration.

2 Empirical Methodology

2.1 The Firm’s Problem

We first introduce a general form of the firm’s production setting. Each of the methods we employ imposes some identifying restrictions on this general model.

Consider firm \(j\) in year \(t\) that produces output \(Y_{jt}\) using capital \(K_{jt}\), labor \(L_{jt}\), and intermediate inputs \(M_{jt}\) according to \(Y_{jt}=F_{j}(K_{jt},L_{jt},\omega ^{M}_{jt}M_{jt})e^{\nu _{jt}}\). Ideally, we would estimate a separate production function \(F_{j}(.)\) for each firm \(j\), but this is infeasible given the short panel. Instead, we group firms with similar technologies as a practical alternative such that all firms \(j\) within a finely defined group \(\mathfrak{g}\) share the same production function, \(F_{j}(.)=F^{\mathfrak{g}}(.)\). We discuss below our strategies to group similar firms.

Hicks-neutral productivity, \(\nu _{jt}=\omega _{jt}+\varepsilon _{jt}\), is composed of (i) a persistent component, \(\omega _{jt}\), which is known to the firm when it makes input decisions in period \(t\), and (ii) a transitory component, \(\varepsilon _{jt}\) (i.i.d. across firms and time with \(\mathbb{E}[\varepsilon _{jt}]=0\)), which is observed after choosing inputs. Changes in these productivity terms may arise from both technology shocks and market demand shifts, while the transitory component may also reflect measurement error in output. Furthermore, \(\omega ^{M}_{jt}\) captures intermediate-augmenting productivity relative to labor, which is persistent over time and is also known to the firm when it makes input decisions. We assume that the persistent productivity components follow a joint exogenous first-order Markov process: \(\mathcal{P}_{\omega}(\omega _{jt},\omega ^{M}_{jt}\,|\,\mathcal{I}_{jt-1})=\mathcal{P}_{\omega}(\omega _{jt},\omega ^{M}_{jt}\,|\,\omega _{jt-1},\omega ^{M}_{jt-1})\), where we define \(\mathcal{I}_{jt}\) as the information set available to firm \(j\) when it makes its decisions in period \(t\).

Inputs that are functions of the previous period’s information set, \(X_{t}(\mathcal{I}_{jt-1})\), are predetermined. Inputs chosen in period \(t\) conditional on \(\mathcal{I}_{jt}\) are variable. We assume capital is predetermined and a state variable \((K_{jt}\in \mathcal{I}_{jt})\), potentially subject to arbitrary adjustment costs and financial constraints; we do not require that firms choose investment optimally.

We assume labor is a dynamic input in that it is a variable input and the firm’s choice of \(L_{jt}\) may depend on its own lagged value, \(L_{jt-1}\in \mathcal{I}_{jt}\). Firms may also face arbitrary labor adjustment costs and possess wage-setting power. As with capital, most of our estimation approaches do not require assumptions on the optimality of the labor choice or the nature of wage setting.

Finally, given the capital and labor choices, firms maximize short-run expected profits by selling their output at a price according to a demand function specific to its group \(\mathfrak{g}\), \(P_{jt}=P^{\mathfrak{g}}_{t}(Y_{jt})\), and buying intermediate inputs in a perfectly competitive market without adjustment costs or other frictions.

2.2 Non-homothetic Production Function: GNR Method

Our main approach builds on the GNR methodology. This technique provides several advantages. First, it identifies output elasticities for gross output, whereas common alternatives (e.g., Ackerberg et al. (2015)) typically only identify value-added technologies. As we show below, variation in the output elasticity of intermediate inputs is a key driver of variation in RTS. Second, its flexible nonparametric approach—approximated in practice via a higher-order polynomial—minimizes specification error when estimating both output elasticities and TFP. Third, the estimated non-homothetic production function, where output elasticities and RTS vary across firms and over time—is crucial for understanding the relationship between firm-level TFP, RTS, and size both between and within groups.

Identifying restrictions. We explain our implementation of the GNR technique in Appendix A and refer to Gandhi et al. (2020) for technical assumptions. Here, we specify the substantive restrictions imposed on the general firm problem: (i) Firms are price takers in the output market, \(P_{jt}=P^{\mathfrak{g}}_{t}\). (ii) There is no intermediate input-augmenting productivity term, \(\omega ^{M}_{jt}=1\). For robustness, in Section 4.3 we employ the method developed in Demirer (2025) to relax these assumptions (at the cost of imposing stronger assumptions on labor input choices and functional form of the production function).

Identification and intuition. GNR provide a rigorous identification proof, to which we refer readers. Here, we focus on the intuition behind our estimation. Because the intermediate input is flexible (i.e., variable and static), the first-order condition (FOC) from the firm’s short-run expected profit maximization implies that the expected intermediate expenditure share equals its output elasticity. Covariation between the (expected) share and input levels then identifies this output elasticity.6 We thus recover the output elasticity of intermediate inputs as a function of input levels via a nonparametric regression of the revenue share of intermediate expenditure on inputs. This regression also identifies the ex-post transitory shock: for two firms with the same input levels, variation in intermediate expenditure shares arises only from differences in ex-post shocks, which manifest through variation in revenues.

With estimates of the intermediate input elasticity and transitory shocks in hand, we remove the effects of intermediates and ex-post shocks from gross output, leaving a residual “value-added” function to estimate in the next step.7 Because capital is predetermined and labor is subject to adjustment costs and input market power, (unknown) wedges arise between expenditure shares and output elasticities, preventing identification of those elasticities via the FOC approach used in the first step. Therefore, our second-stage estimation follows the proxy-variable literature (Olley and Pakes (1996)) in exploiting Markov timing assumptions on the persistent shock to form GMM conditions. Intuitively, conditional on the previous period’s persistent productivity (\(\omega _{jt-1}\)), covariation between residual value added and capital and labor inputs identifies their output elasticities, with lagged labor serving as an instrument for current labor. Similarly, conditional on inputs and \(\omega _{jt-1}\), variation in value added identifies the persistent shocks. Thus, a high-RTS firm is characterized by a high intermediate input expenditure share, a strong correlation between output and capital or labor, or both, whereas a high-TFP firm exhibits greater value added for given inputs and their elasticities.

Cobb-Douglas with RTS heterogeneity. The baseline GNR approach allows for a nonparametric production function. To investigate whether our findings are sensitive to this flexible functional form, as a special case, we impose homogeneous relative output elasticities—within each group \(\mathfrak{g}\)—while allowing for heterogeneity in RTS: \(F_{jt}(K_{jt},L_{jt},M_{jt})=\left (K^{\varepsilon ^{\mathfrak{g}}_{K}}_{jt}L^{\varepsilon ^{\mathfrak{g}}_{L}}_{jt}M^{\varepsilon ^{\mathfrak{g}}_{M}}_{jt}\right)^{\eta _{jt}}\).8 The other assumptions remain as in the baseline specification. We follow the same two-step estimation procedure and identify firm-year level \(\eta _{jt}\) in the first stage from variation in intermediate input expenditure shares.

2.3 Clustering firms

Estimating a firm-specific production function \(F_{j}(.)\) is infeasible given the short panel of our data sets. We therefore implement these methods at the group level \(\mathfrak{g}\), pooling firms that operate under similar technologies. The key empirical challenge is how to define such groups so that firms with comparable production technologies are grouped together to share a common technology while allowing for systematic technological heterogeneity across firms.

Our baseline estimates apply the GNR method within 2-digit industries, assuming firms in industry \(\mathfrak{i}\) share a common nonparametric production function \(F^{\mathfrak{i}}(.)\). Even under this restriction, firms within industries differ in their factor elasticities—and thus in RTS—because they operate at different points in the input space of a non-homothetic technology. We show below that these differences are highly persistent over time, suggesting that they reflect stable technological differences across firms rather than transitory input choices.

To further investigate whether RTS heterogeneity stems from ex-ante firm differences rather than local elasticity variation from non-homotheticity, we also estimate cluster-specific production functions within industries. Within each industry, we employ an iterative clustering procedure using a k-means algorithm. Firms are initially grouped based on their baseline average RTS estimates over the sample period. Cluster assignments are constrained to be constant over a firm’s life cycle, consistent with our interpretation that clusters capture persistent production technologies. We then re-estimate cluster-specific non-homothetic production functions employing the GNR method, update firm-level RTS estimates, and reassign firms to clusters based on these updated values. This process repeats until the estimated RTS–size relationship converges.

This approach generates two sources of RTS variation across firms: (i) within-cluster variation due to non-homotheticities, and (ii) between-cluster variation, arising from fundamentally different technologies across clusters. This distinction also allows us to quantify the relative importance of technology heterogeneity versus TFP differences in explaining the firm size distribution. For robustness, in Appendix B we also report results using two simpler and more transparent approaches, grouping firms directly based on observable characteristics such as input shares and firm size.

3 Data and Sample Selection

Our main dataset is the Canadian Employer-Employee Dynamics Database of Statistics Canada (CEEDD), a set of linkable administrative tax files covering the universe of tax-paying Canadian firms and individuals from 2001 to 2019. We obtain balance sheet and income statement information from the National Accounts Longitudinal Microdata File, which covers all incorporated firms.9 Revenue and wage bill variables are constructed by Statistics Canada based on corporate tax return line items and are consistent with the national income and product accounts. We construct total tangible capital using the perpetual-inventory method (PIM), starting from the first book value observed in the data, annual tangible capital investment, and amortization. Intermediate inputs are calculated as the sum of operating expenses and costs of goods sold net of capital amortization. All nominal values are deflated to 2002 real Canadian dollars. See Appendix C.1 for further details and summary statistics (Table A.2).

To construct the estimation sample, we start from firm-year observations with nonmissing values for revenue, capital, wage bill, intermediate inputs, and industry code. To ensure reliable PIM capital estimates, we include only observations with at least two prior years of capital data. We further drop observations with outlier factor shares: (i) wage-bill-to-revenue or wage-bill-to-value-added ratios below the 1st or above the 99th percentile; (ii) intermediate-input-to-revenue ratios outside \([0.05,0.95]\); and (iii) capital-to-revenue ratios above the 99.9th percentile. After sample selection, our dataset comprises 4.3 million firm-year observations and 620,000 firms, with an average of 6.9 observations per firm.

U.S. manufacturing sector. As a robustness exercise, we conduct a similar analysis using data from the U.S. Economic Census and the Annual Survey of Manufactures (ASM), widely used in the literature on firm-level productivity in the U.S. (e.g., Foster et al. (2001) and Bloom et al. (2018)). This dataset contains detailed information on over 60,000 manufacturing plants between 1974 and 2019. Unlike our Canadian data, it does not cover the full universe of firms but a representative panel of manufacturing plants, redrawn every five years. We restrict the sample to plants with at least two years of nonmissing data for key variables, resulting in 3.1 million establishment-year observations. Revenue is measured by the total value of shipments. The Census also reports real capital stock (measured using the PIM), total wages of all plant workers, and expenditures on intermediate inputs, all expressed in 2019 U.S. dollars. We discuss additional details in Appendix C.2.

Moody’s Orbis dataset. We further complement our analysis using data from eleven European countries including Germany, France, Italy, and Spain. This dataset provides harmonized information on revenues, wage bill, capital stock, and intermediate inputs (all in 2019 prices) for a large sample of private and public firms across industries. For most countries, data coverage spans 2005–2019.10 See Appendix C.3 for additional details.

| Mean | St. dev | P10 | P50 | P90 | P99 | ||

| Panel A: Main Estimates | |||||||

| TFP | — | 0.17 | –0.18 | 0.00 | 0.17 | 0.52 | |

| RTS | 0.96 | 0.04 | 0.92 | 0.95 | 1.00 | 1.08 | |

| Panel B: Output Elasticities | |||||||

| Intermediates | 0.59 | 0.15 | 0.42 | 0.59 | 0.78 | 0.99 | |

| Labor | 0.33 | 0.15 | 0.14 | 0.33 | 0.50 | 0.66 | |

| Capital | 0.04 | 0.03 | 0.00 | 0.03 | 0.08 | 0.13 | |

| Panel C: Input Shares | |||||||

| Intermediates | 0.61 | 0.18 | 0.36 | 0.61 | 0.85 | 0.93 | |

| Labor | 0.29 | 0.15 | 0.11 | 0.28 | 0.50 | 0.72 | |

| Capital | 0.03 | 0.07 | 0.00 | 0.01 | 0.08 | 0.32 | |

Notes: Table I shows cross-sectional moments of the distributions of firm-level log TFP, RTS, and the elasticities of output with respect to intermediate inputs, labor, and capital. To obtain these estimates, we apply our baseline method (GNR) within two-digit NAICS and calculate the cross-sectional moment within the same cell. Then we average across all estimated values weighting by the number of observations in each cell. The total number of observation is 4.3 million firm-years. To compare TFPs across industries, we normalize its median to zero within each industry.

4 Empirical Results: RTS versus TFP Differences

Our baseline results are obtained by applying the GNR methodology to each of the 23 two-digit NAICS industries in the Canadian administrative data, estimating the output elasticities of inputs and TFP for all firm-year observations (see Table A.10 for the list of industries and summary statistics). We begin by presenting the variation in output elasticities—and thus RTS—and TFP within industries (see Table I).11 We also highlight key data features that illustrate the identification argument underlying this variation.

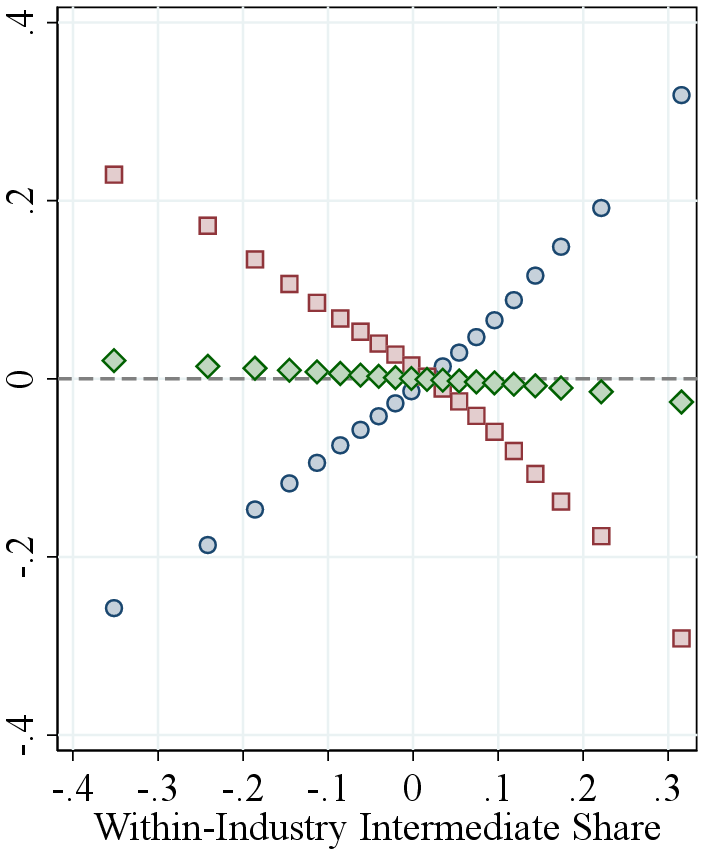

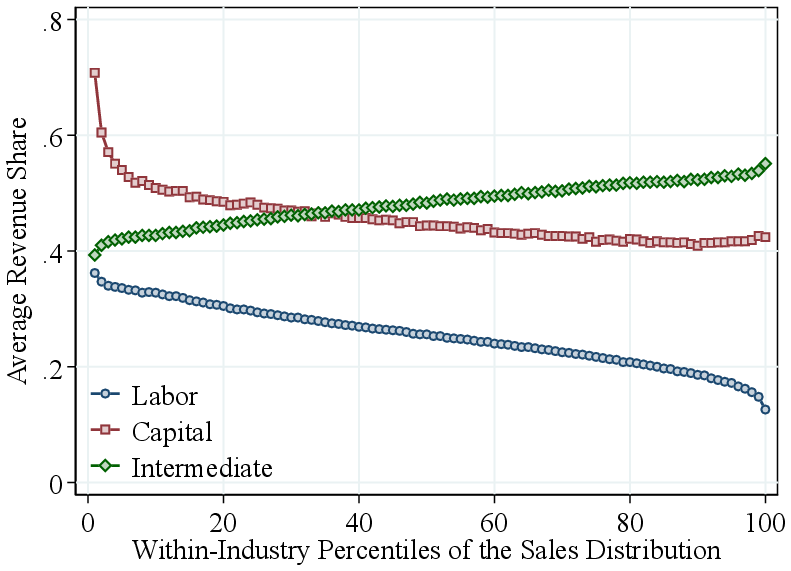

Notes: Figure 1 shows the relation between the input revenue shares defined as the ratio between the total cost of intermediate inputs, the total wage bill, and the total value of capital stock, divided by firm revenue, and the estimated output elasticity. Firms are ordered by the respective factor shares on the horizontal axis. The vertical axis shows averages of estimated output elasticities, demeaned within two-digit NAICS industry.

RTS heterogeneity. The within-industry RTS distribution has an average of 0.96 and a \(90^{th}\)-to-\(10^{th}\) percentile gap (P90–P10) of 0.08.12 This implies that the output response to a given proportional increase in inputs is about 8.3% larger for a firm at the \(90^{th}\) percentile of RTS than for a firm at the \(10^{th}\) percentile, holding TFP constant. These differences are quantitatively important when interpreted as deviations from constant returns to scale. In an efficient economy with Cobb-Douglas production, the elasticity of optimal firm output to firm TFP is \(\frac{1}{1-RTS}\). This elasticity is five times larger for a firm with RTS of 0.98 compared to one with RTS of 0.90.13 RTS dispersion is more pronounced above the median: the average within-industry P50–P10 is 0.03 compared to 0.05 for P90–P50 and 0.13 for P99–P50. The average 90th percentile for RTS across industries is 1.00; that is, most firms operate decreasing returns to scale technologies, yet some exhibit annual RTS above 1. 14

By construction, differences in RTS arise from heterogeneity in output elasticities. Intermediate inputs have the highest average output elasticity at 0.59, followed by labor at 0.33 and capital at 0.04 (Panel B of Table I).15 Labor and intermediate input elasticities also show larger within-industry variation than capital elasticities, with average P90-P10 gaps of 0.36 for intermediates and labor versus 0.08 for capital. Variance decompositions show that over 60% of the variation in each output elasticity is explained by within-industry differences, compared to only about 25% for RTS (Table A.11). This discrepancy reflects the negative correlation between output elasticities within industries (Table A.12).

Output elasticities and input shares. Following the identification argument in Section 2.2, we now present the key data features underlying our estimates. In models with competitive markets, output elasticities are equal to input revenue shares for flexible inputs. Our specification is more general, and the GNR method does not rely solely on the FOCs of profit-maximizing firms. Nevertheless, estimated output elasticities are positively correlated with the corresponding factor shares with similar levels. (Panels B and C of Table I).

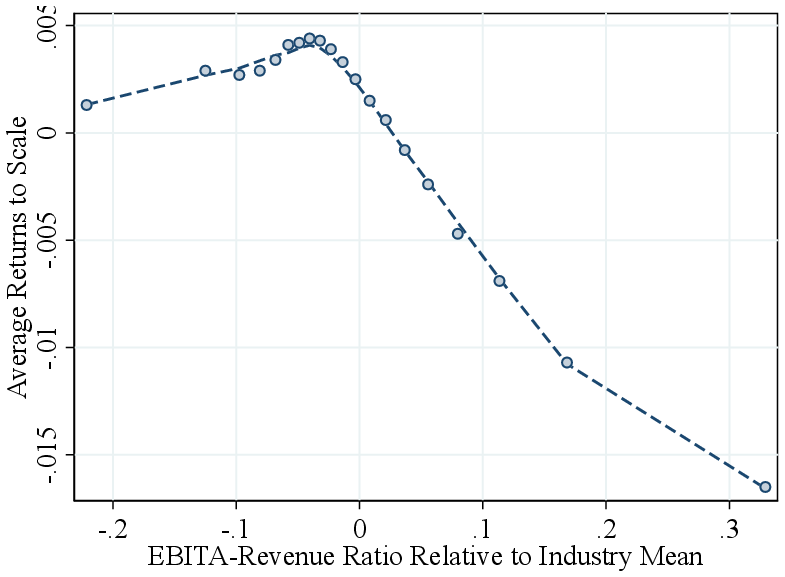

Each panel of Figure 1 shows a bin scatter of (demeaned) output elasticities for all three inputs against a different input share. Across all inputs, elasticities are strongly positively correlated with their respective shares: intermediate input-intensive firms have higher intermediate input elasticities, labor-intensive firms have higher labor elasticities, and capital-intensive firms have higher capital elasticities. The relationship is strongest for intermediate inputs, consistent with our estimation approach, which treats intermediates as flexible and uses firms’ FOCs to estimate their elasticities. For labor and capital, our estimation does not rely on FOCs, yet we still observe strong correlations. These patterns support the identification intuition in Section 2.2: heterogeneity in output elasticities—and thus in RTS—largely reflects differences in input shares. They also suggest that high-RTS firms should have relatively low profit shares, which we confirm in the data by showing a negative correlation between the EBITDA-to-revenue ratio and RTS across firms (Figure A.7).

TFP dispersion. The average within-industry P90-P10 gap for TFP is 0.35, implying that a firm at the \(90^{th}\) percentile produces about 41.9% more output than a firm at the \(10^{th}\) percentile, conditional on inputs and output elasticities. This gap is substantially smaller than previous estimates even for narrow six-digit industries in Canada and the U.S., where typical P90-P10 TFP gaps are about twice as large (e.g., De Loecker and Syverson (2021) and Syverson (2011)). Two factors explain the difference: first, we estimate a flexible nonparametric production function that allows for differences in RTS; second, we use the wage bill rather than headcount or hours as the measure of labor input (see Fox and Smeets (2011)).

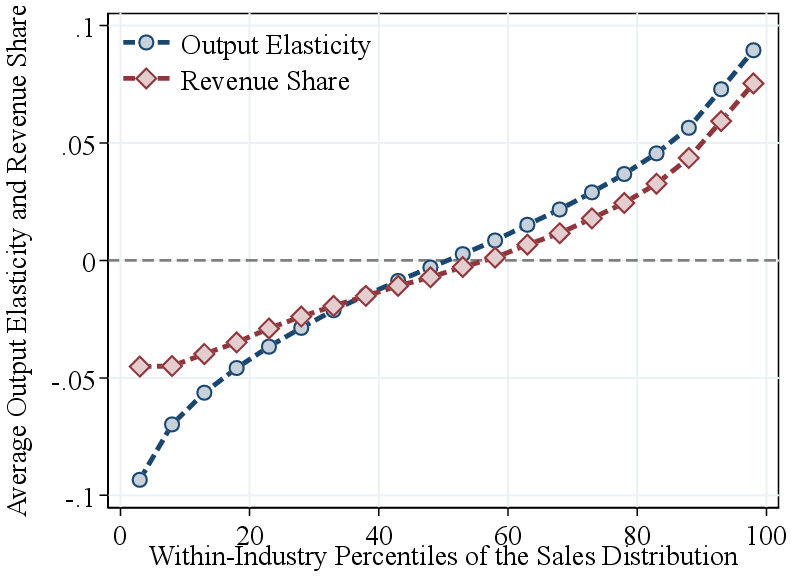

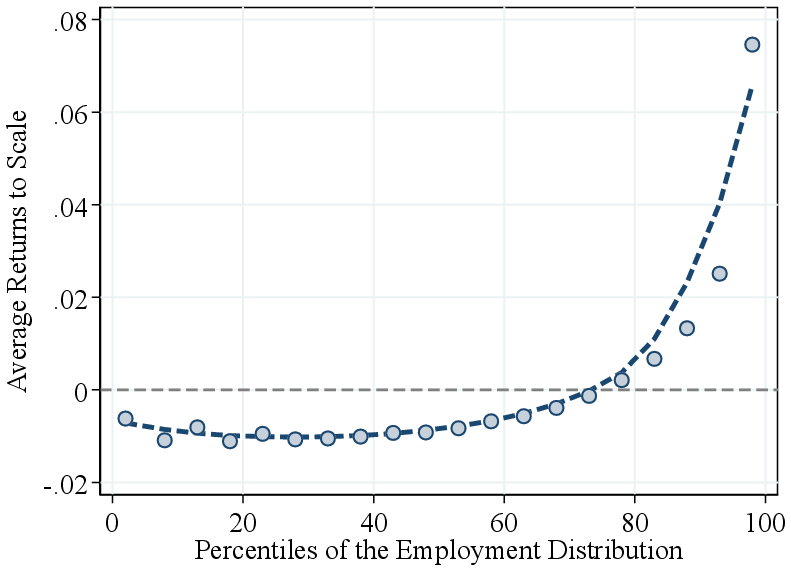

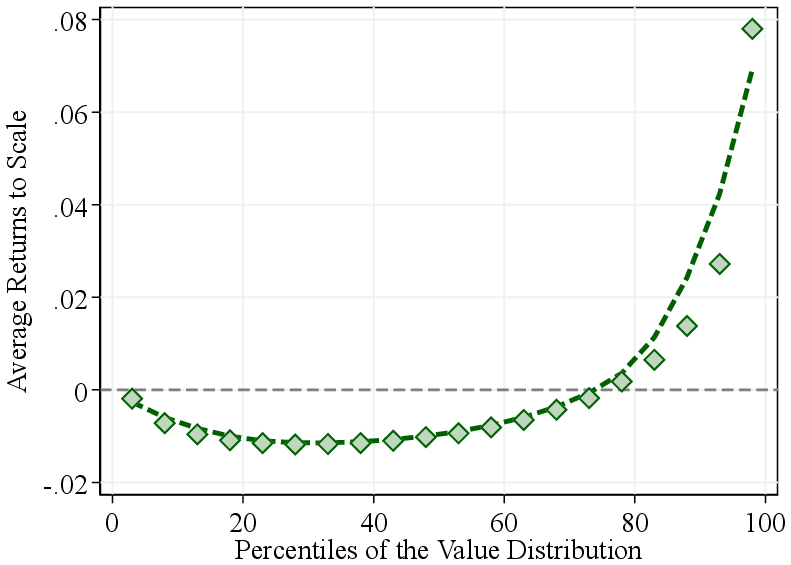

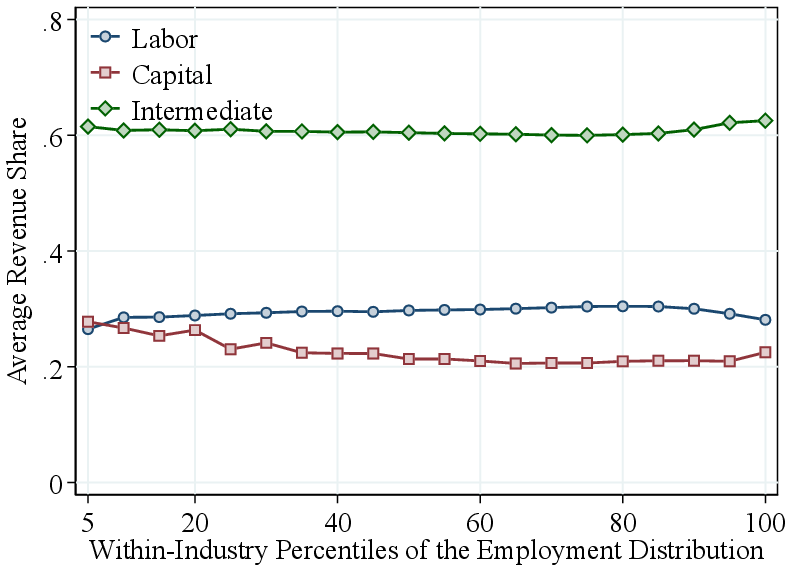

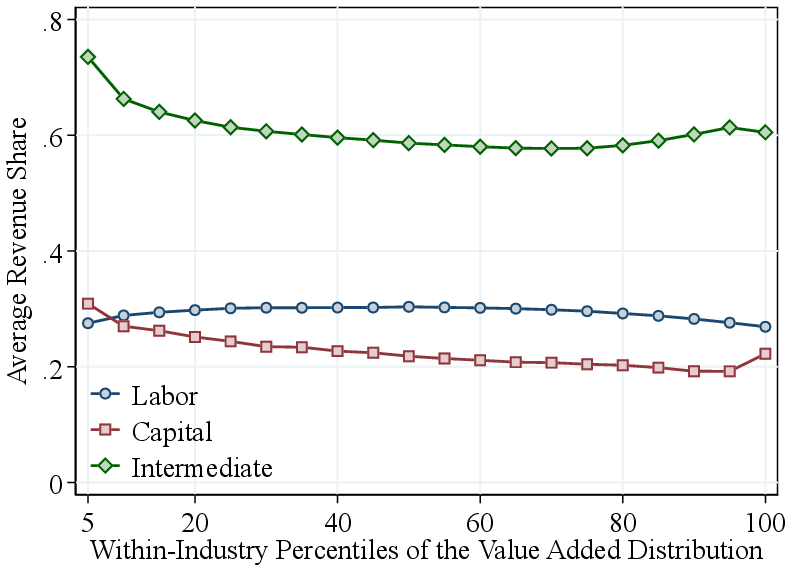

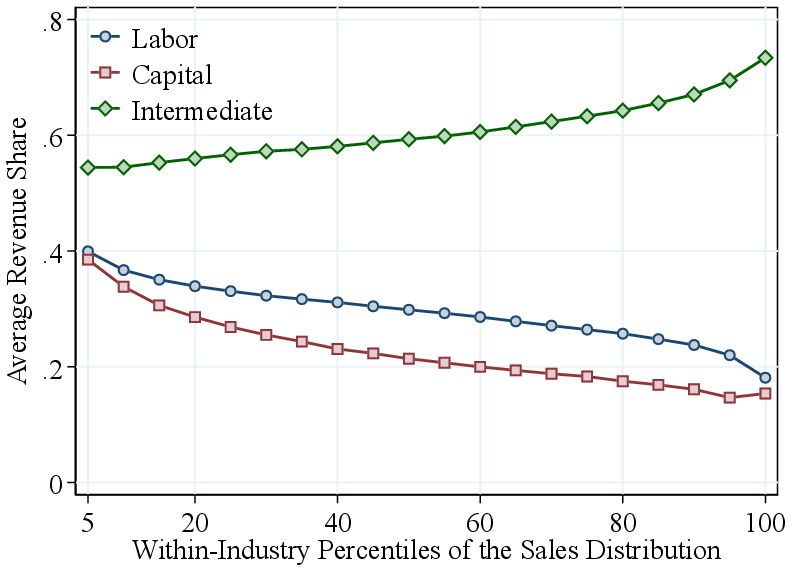

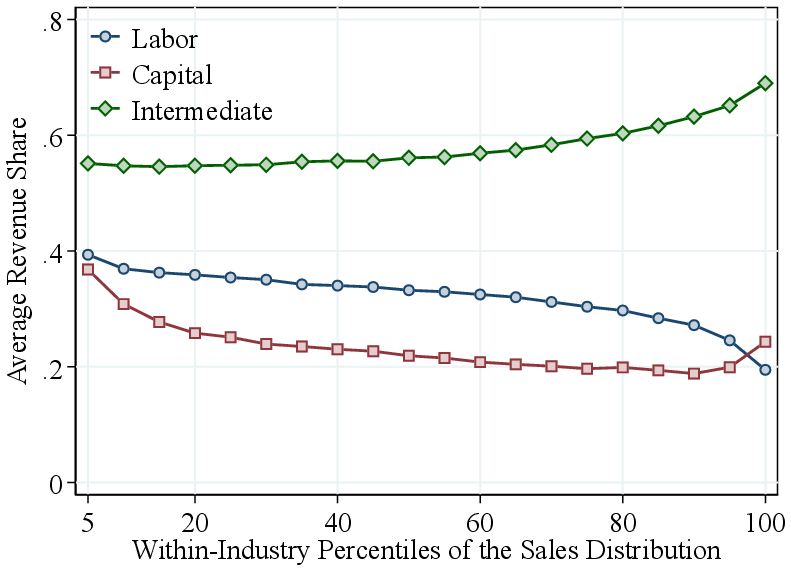

Notes: Figure 2a shows the average RTS across quantiles of the firm-revenue distributions, using both pooled and within-industry percentiles. RTS is demeaned by the pooled average (average RTS of 0.96) in the former and by industry averages in the latter. Figure 2b presents the estimated output elasticity and the observed revenue share of intermediate inputs, both demeaned by industry averages, across quantiles of the within-industry revenue distribution.

We next examine how RTS and TFP vary across the firm-size distribution. Section 4.2 presents our clustering results on ex-ante heterogeneity in firm technologies. Sections 4.3 and 4.4 show that our key result on RTS heterogeneity is robust to alternative estimation methods and samples. Finally, we relate our findings to broader debates on firms’ life-cycle growth and on wage and wealth inequality in Section 4.4.

4.1 Production Technologies over the Firm-Size Distribution

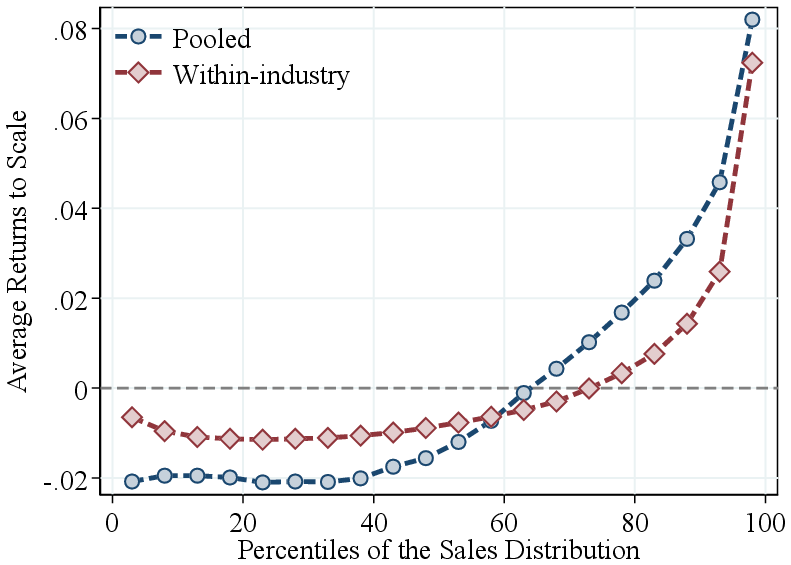

Returns to scale by firm revenue. We now turn to the systematic variation in RTS across the firm revenue distribution. To this end, we pool all firm-year estimates from 23 two-digit NAICS industries. Figure 2a shows bin scatter plots of (demeaned) average RTS by firm revenue using two ranking methods. First, we pool firm-year observations across all industries and rank them into revenue percentiles. We find that RTS is relatively flat across the bottom two-fifths of firms but increases sharply for larger firms in the economy. Average RTS rises by about 10 p.p. from the bottom to the top of the revenue distribution, primarily above the median.

Part of the variation in our pooled ranking may reflect differences across industries. For example, manufacturing firms, which tend to have higher RTS and larger revenues, are overrepresented at the top. Therefore, to isolate within-industry patterns, we calculate within-industry revenue percentile rankings. This approach reveals similar patterns: RTS is roughly constant below the median and increases steeply among larger firms within industries, with an 8 percentage point gap between the top 5% and the bottom half. Thus, most of the observed variation in RTS by firm size is driven by differences within industries, rather than across industries.

Output elasticities by firm revenue. Our analysis shows that the positive relationship between RTS and firm revenue is entirely driven by the intermediate input elasticity (Figure 2b). The intermediate input elasticity increases monotonically from -0.09 (relative to the industry average) for firms in the bottom 5% of the revenue distribution, to approximately zero around the median, and up to 0.09 for firms in the top 5%. This 9 p.p. gap in intermediate input elasticities between the top 5% and median firms fully explains the corresponding 8 p.p. gap in RTS over the same range. Figure 2b also shows that the intermediate input revenue share mirrors this pattern, with larger firms allocating a higher share of their revenue to intermediate inputs compared to smaller firms. This result is expected, as our estimation treats intermediate inputs as a flexible factor.16 Consistent with our findings, in a contemporaneous study Mertens and Schoefer (2025) use a setting with homothetic production functions and imperfect input markets to show that firms grow by shifting from labor to intermediate inputs. Finally, capital and labor elasticities decline slightly with firm revenue (Figure A.4), underscoring the importance of estimating gross output production functions: relying on value-added specifications may lead to misleading conclusions about firm-level technologies.

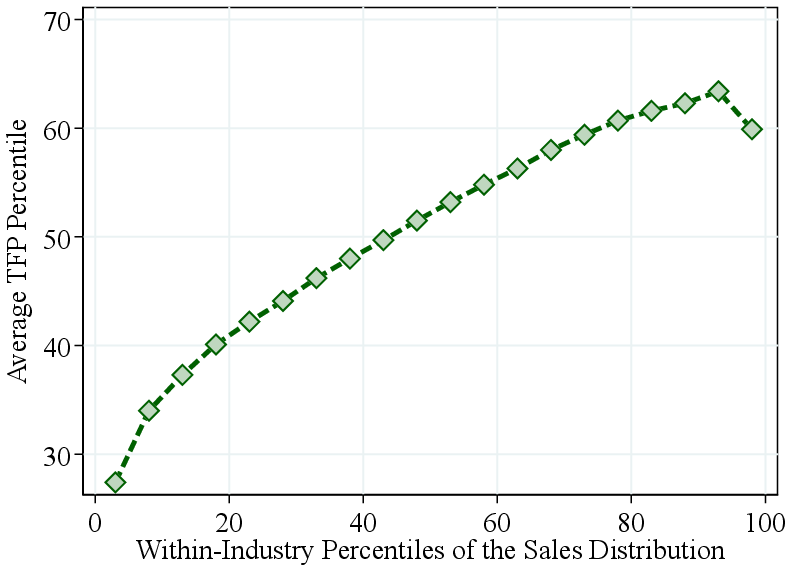

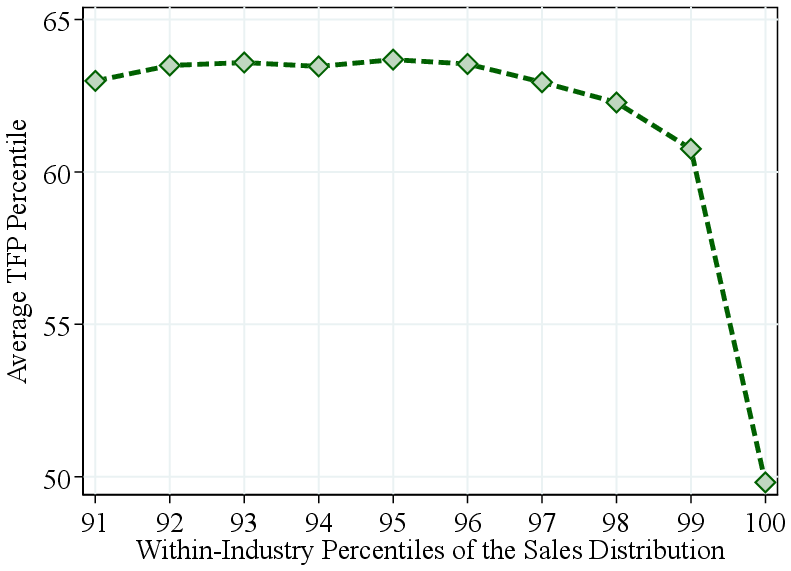

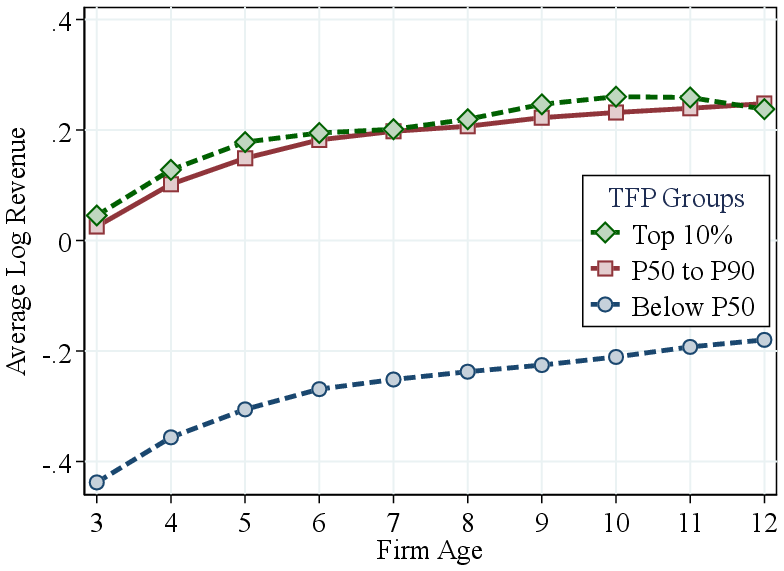

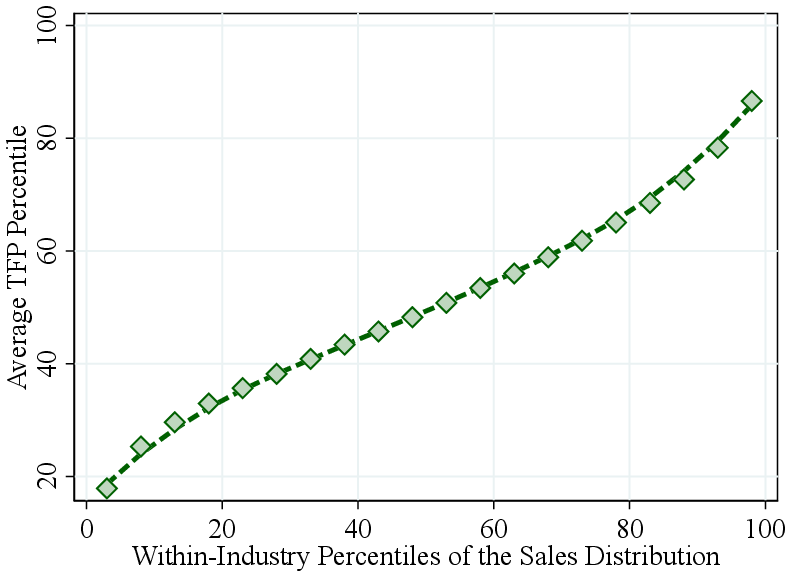

Notes: Figure 3a shows the average firm TFP rank within percentiles of the within-industry revenue distribution. The TFP rank is calculated within each industry. Figure 3b zooms in on the top 10% of the revenue distribution.

Total factor productivity by firm revenue. We next investigate whether larger firms also exhibit higher TFP. Since TFP levels are not comparable across industries, we focus on firms’ relative productivity ranks within industries. Figure 3a displays the average within-industry TFP percentile by within-industry revenue percentile.

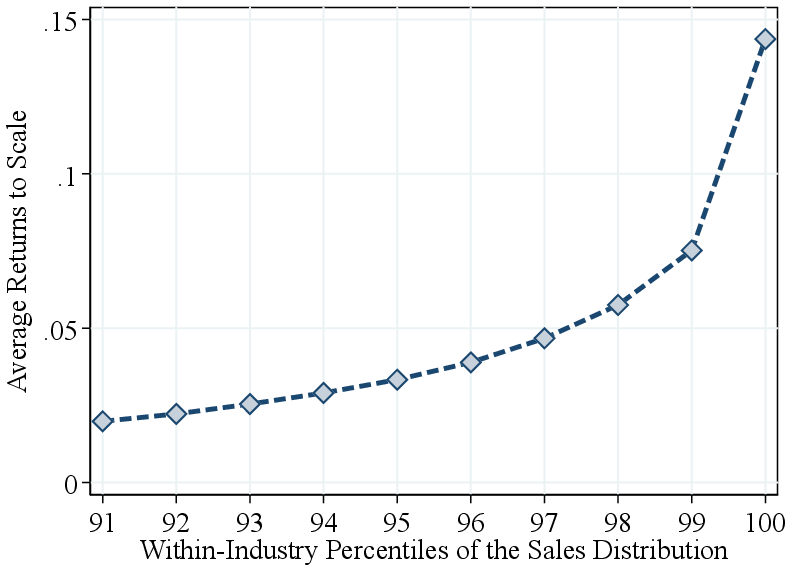

We find that relative TFP increases with firm size up to the top decile of the revenue distribution, after which it flattens out. In fact, zooming in on the top 10%, we find that TFP falls off sharply for the largest firms (Figure 3b). In contrast, RTS increases even more steeply among the largest firms (Figure A.8). Thus, the largest firms tend to feature the highest RTS—not necessarily the highest TFP—as commonly assumed.

A few papers have studied the TFP-size relation (see Leung et al. (2008) or Baldwin et al. (2002)). Our results on the TFP-revenue gradient differ from these studies because we allow for heterogeneity in production technologies. To illustrate this, we reestimate a standard Cobb-Douglas production function imposing homogeneous RTS: \(Y_{jt}=e^{\nu _{jt}}K^{\alpha _{i}}_{jt}L^{\beta _{i}}_{jt}M^{\gamma _{i}}_{jt}\), where \(j\) and \(i\) denote firms and industries, respectively. As expected, under this restriction TFP increases monotonically with firm size (Figure A.10). This contrast highlights the importance of allowing for flexible production technologies in understanding the relationship between firm-level TFP, RTS, and size.

4.2 Ex-ante Technology Differences

Our benchmark GNR method estimates a flexible but common production function across firms within an industry, allowing output elasticities to vary with each firm’s input bundle. A central question is how much of the observed RTS dispersion reflects permanent differences in production technologies across firms versus non-homothetic variation along a common production function. For example, did a large, high-RTS firm also possess a more scalable technology when it first entered the industry as a smaller firm? We present three complementary pieces of evidence—ranging from transparent descriptive patterns to cluster-based production function estimates—all pointing to the same conclusion: the bulk of RTS heterogeneity reflects persistent technological differences across firms rather than non-homothetic variation along a common production function.

4.2.1 Persistence in Local Elasticities

Fixed effects regression. First, we regress RTS estimates from our baseline GNR method on firm size, firm age, time dummies, and firm fixed effects. If differences in RTS are largely permanent, firm fixed effects should absorb most of the variation. This is exactly what we find: of the total RTS variance of \(0.052^{2}\), firm fixed effects (with a variance of \(0.045^{2}\)) account for 75% of the variation when controlling for firm age and size. We find similarly strong persistence in U.S. manufacturing: RTS has a variance of \(0.058^{2}\) and fixed effects account for 65% of the total variation after controlling for other firm observables.

Autocovariance structure. Second, following the earnings dynamics literature (e.g., Abowd and Card (1989); Karahan and Ozkan (2013)), we use the autocovariance structure of RTS estimates to decompose firm-level RTS into a firm-specific fixed effect, a persistent AR(1) component, and a fully transitory component (see Appendix D for details). Consistent with the fixed effects results, only 10.5% of the total RTS variance is attributable to purely transitory shocks. Firm fixed effects and the highly persistent component (with an estimated persistence parameter of 0.94) account for 38.9% and 50.6% of the total variation, respectively.

4.2.2 Permanent Technological Differences: Clustering Analysis

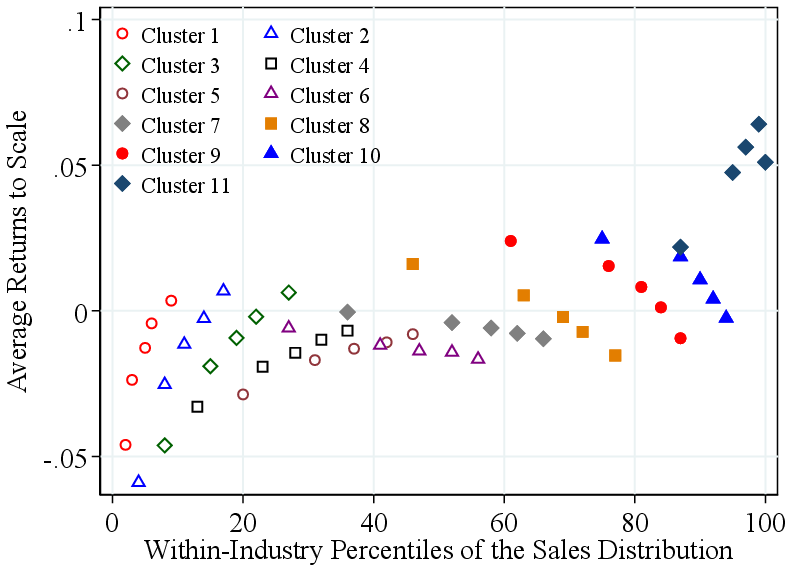

These persistence results are consistent with two interpretations: firms may operate genuinely different production technologies, or they may share a common non-homothetic technology but maintain persistently different input bundles—for instance, due to financial constraints or other frictions. To distinguish between these interpretations, we turn to cluster-specific production function estimation. As detailed in Section 2.3, we implement an iterative clustering procedure that groups firms with similar technologies. Since cluster assignments are constant over each firm’s life cycle, this approach directly asks whether today’s large, high-RTS firms operated a more scalable technology even when they were small. The resulting RTS gap between the top and bottom deciles is 7.6 p.p.—larger than the baseline gap of 5.7 p.p.—reflecting the additional flexibility that cluster-specific production functions afford relative to the common-technology benchmark (Figure 4).

The clustering framework allows us to separate (i) within-cluster RTS variation driven by non-homotheticities along a common technology from (ii) between-cluster RTS variation, reflecting genuine technology differences. To isolate the technology component, we replace firm-level RTS with the corresponding cluster-average RTS. The P90-P10 RTS gap declines only modestly, from 7.6 p.p. to 6.3 p.p., implying that 83% of the observed dispersion reflects differences in production technologies rather than non-homotheticities along a common production function. Crucially, the resulting clusters are not simply partitions of the input space: firms in different clusters overlap substantially in their input usage, confirming that the between-cluster RTS differences reflect genuinely distinct technologies.

Notes: Baseline reports RTS estimated from the baseline GNR specification with a common production function within industries. Clustering reports RTS from the iterative clustering procedure that groups firms with similar technologies and estimates cluster-specific production functions using the GNR method. Cluster Average replaces firm-level RTS with the corresponding cluster-level mean RTS.

Our results are robust to alternative ways of grouping firms. Appendix B reports estimates using two simpler clustering schemes based on input shares and firm size. First, given the importance of input shares in identifying factor elasticities, we cluster firms within industries based on input shares and revenue percentiles over their lifecycle. Second, to capture persistent technology differences across firms with different growth trajectories, we group firms by their maximum revenue percentile attained over their life cycle. Across these alternative classifications, the RTS–size gradient and the implied RTS gaps remain similar to our baseline estimates, with most RTS dispersion reflecting persistent differences across clusters rather than variation along a common technology.

Taken together with the persistence evidence from the fixed-effects regressions and the autocovariance analysis, these results indicate that most RTS heterogeneity reflects ex-ante technological differences across firms rather than transitory variation in local elasticities. These findings are consistent with the endogenous entrepreneurship model with heterogeneous RTS in Section 5.

Accounting for Firm Size: Technology versus TFP Differences. A natural question is how much of the within-industry firm-size distribution reflects differences in technology (RTS) versus differences in productivity (TFP). Answering it requires addressing two conceptual challenges.

First, we need genuine between-firm technology heterogeneity, not merely local elasticity variation from firms operating at different points along a common non-homothetic production function. Our iterative-clustering approach directly addresses this issue by estimating separate production functions for groups of firms with similar technologies. To construct the counterfactual, we define a common technology within each industry as the coefficient-wise average of the cluster-level production functions.17 Under this common technology, firms share the same production function but differ in TFP; allowing cluster-specific production functions, by contrast, captures technology heterogeneity across firms.

A second complication is that TFP levels are not directly comparable across technologies. We therefore normalize TFP to have mean zero within each cluster, so that firm-level TFP captures productivity relative to the cluster average. Differences in mean TFP across clusters—the production function intercept—are attributed to technology heterogeneity.

We then construct counterfactual revenues for each firm-year observation by successively imposing common TFP, common technology, or both. A Shapley–Owen decomposition exercise shows that technology heterogeneity accounts for the majority of firm-size dispersion within industries: it explains 68%, 73%, and 71% of the p99–p50, p95–p50, and p90–p50 revenue gaps, respectively. The remaining dispersion is, by construction, explained by TFP differences. These patterns reinforce the paper’s central finding: the size advantage of large firms primarily reflects the technology they operate rather than higher productivity within a common technology.

4.3 Robustness of Results

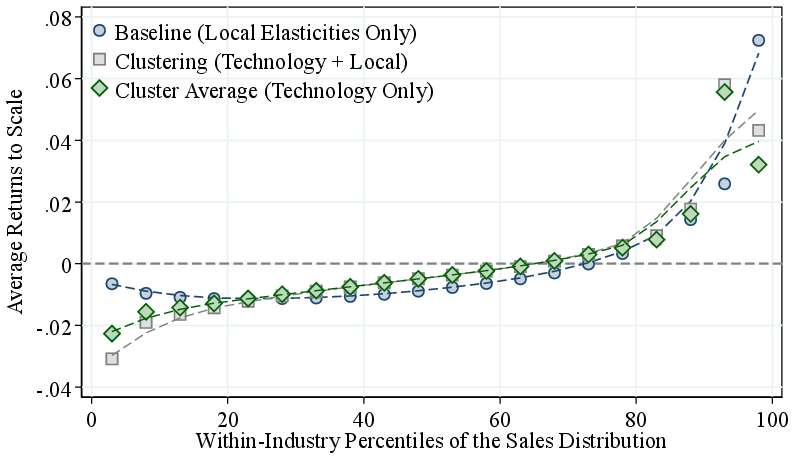

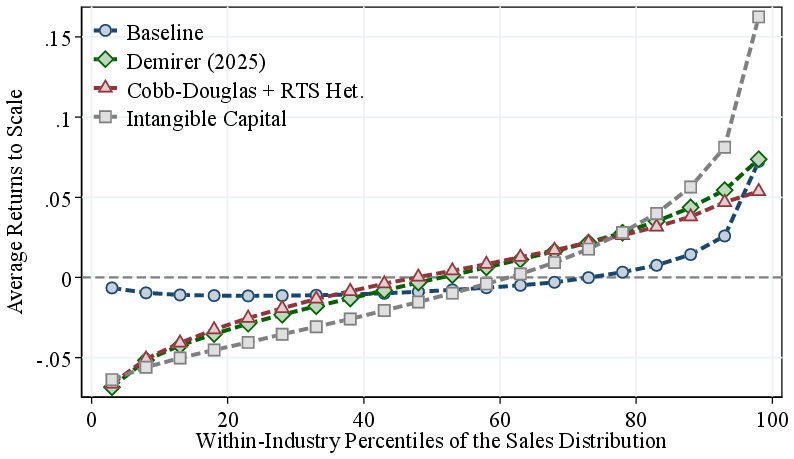

Our benchmark method, GNR, relies on several identifying assumptions, such as firms being price takers in output markets. In this section, we relax some of these assumptions and apply alternative methods to show that our key result—larger firms operate technologies with higher RTS—is robust. If anything, these alternative specifications imply an even steeper RTS–size gradient, strengthening our main result (Figure 5).

Notes: In the intangible capital specification, we include intangible assets, constructed using PIM, into the capital stock measure and apply the GNR method. In all specifications, we sort firms based on revenue within industry, and RTS is demeaned by industry averages.

4.3.1 Markups and Market Power

Our RTS estimates are based on revenue elasticities of the three inputs. A key concern in the literature (e.g., Bond et al. (2021)) is that identifying revenue-based or physical production functions typically requires either price and quantity data or strong parametric assumptions about demand and technology. In particular, using revenue data alone may lead to unknown biases in estimates of markups and output elasticities. However, recent evidence (e.g., De Ridder et al. (2022)) suggests that such biases are modest in practice and that relative variation in markups and elasticities is well identified even with revenue-based data. Consistent with this view, we show that relative variation in RTS—our main object of interest—is robust across multiple estimation methods. Specifically, we present three sets of theoretical and empirical arguments supporting our interpretation that the observed positive relationship between RTS and firm size primarily reflects technological differences, rather than variation in markups (e.g., De Loecker et al. (2020)), or monopsony markdowns (e.g., De Loecker et al. (2016) and Burstein et al. (2024)).

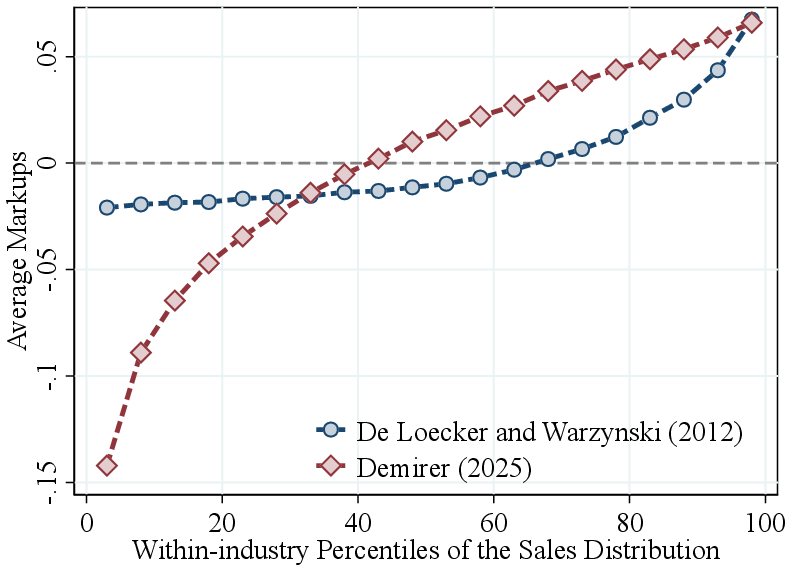

Role of markups. First, if larger firms charge higher markups or markdowns—as implied by models with oligopolistic competition (e.g., Atkeson and Burstein (2008)) or monopolistic competition under log-concave demand systems (e.g., Edmond et al. (2023))—then physical RTS would increase even more strongly with firm size than revenue-based RTS. This follows because the physical output elasticity equals the revenue elasticity multiplied by the firm’s markup. We directly estimate firm-level markups following De Loecker and Warzynski (2012) and find that markups increase with firm revenue in our data (Figure A.3)—consistent with De Loecker et al. (2020)— indicating that the size gradient is larger for physical RTS than for revenue-based RTS.

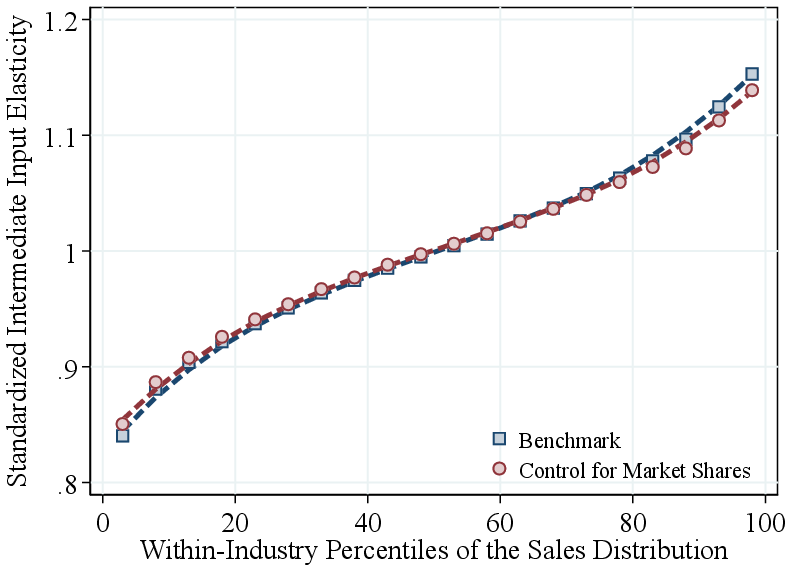

Controlling for market power. Second, while our baseline method permits markdowns in capital and labor markets, it does not account for markups in output markets or markdowns on intermediate inputs. We then extend the GNR approach to explicitly control for both types of market power using firms’ output market shares as proxies for unobserved price elasticities (following De Loecker et al. (2020) and De Loecker et al. (2016)). Relaxing the perfect competition assumption, we allow firms to face downward-sloping demand and adjust the FOC for intermediate inputs accordingly.18 If markups (or markdowns) are a significant determinant of input expenditure shares, we should find that our estimates of the intermediate input elasticity are sensitive to the inclusion of these controls. Controlling for market share barely changes the size gradient of the intermediate input elasticity (Figure A.12), the main driver of RTS differences along the firm-size distribution.

Demirer method. Third, we apply Demirer (2025)’s method, which explicitly allows for heterogenous markups across firms. Yet, it requires several stronger assumptions on production and input choices. Specifically, we impose the following restrictions on the general firm problem (Section 2.1): (i) Firms \(j\) in industry \(\mathfrak{i}\) share a common, weakly homothetic separable production function \(F^{\mathfrak{i}}(K_{jt},h^{\mathfrak{i}}(L_{jt},\omega ^{M}_{jt}M_{jt}))\) where \(h^{\mathfrak{i}}\) is homogeneous in both inputs and \(\omega ^{M}_{jt}\) is intermediate-augmenting productivity. (ii) Both \(M_{jt}\) and \(L_{jt}\) are flexible inputs, optimally chosen, and firms are price takers in both input markets. (iii) Firms have price setting power in output markets via a demand function \(P_{jt}=P^{\mathfrak{i}}_{t}(Y_{jt})\). See Demirer (2025) for additional technical assumptions.19

Under these different assumptions, the estimated RTS-size gradient remains robust and, if anything, becomes even steeper: RTS increases by about 10 percentage points from the bottom half to the top 5% of the firm-size distribution (Figure 5). These results are consistent with the view that physical RTS increases more strongly with firm size than revenue-based RTS, as expected if markups increase with firm revenue—a relationship we confirm again using the Demirer methodology (Figure A.3).

Factor-augmenting productivity shocks. Another potential concern is that larger firms may have higher intermediate input elasticities simply because they use intermediate inputs more efficiently, reflecting factor-specific productivity shocks. Since our results remain robust under Demirer (2025)’s method, which accommodates factor-augmenting productivity shocks, this concern is likewise alleviated.

4.3.2 Cobb-Douglas with RTS Heterogeneity.

Another potential concern is that our results may be sensitive to the flexible functional form assumed in the GNR method. To address this, we reestimate the production function by imposing homogeneous relative factor elasticities while still allowing for RTS differences, i.e., \(F_{jt}(K_{jt},L_{jt},M_{jt})=\left (K^{\varepsilon _{K}}_{jt}L^{\varepsilon _{L}}_{jt}M^{\varepsilon _{M}}_{jt}\right)^{\eta _{jt}}\). Consistent with our baseline findings, the Cobb-Douglas series in Figure 5 shows that RTS increases with firm size by about 10 p.p., with a steeper rise in the bottom half of the revenue distribution and a more moderate increase among the largest firms relative to our baseline.

4.3.3 Intangible capital.

We also analyze the importance of including intangibles in our measure of firms’ capital stock and reestimate their production functions using Canadian data. In theory, including intangibles affects measured productivity, the output elasticity of capital, and therefore RTS. In particular, if larger firms invest disproportionally more in intangible capital, omitting intangibles would understate their capital elasticity (and thus RTS) and overstate their TFP. Consistent with this intuition, we find that the positive relationship between firm size and RTS becomes even stronger when intangible capital is included. As shown in Figure 5, the P95–P50 RTS gap increases from \(0.08\) in the baseline to \(0.20\) when intangible capital is incorporated.

4.3.4 Ranking firms by employment or value added.

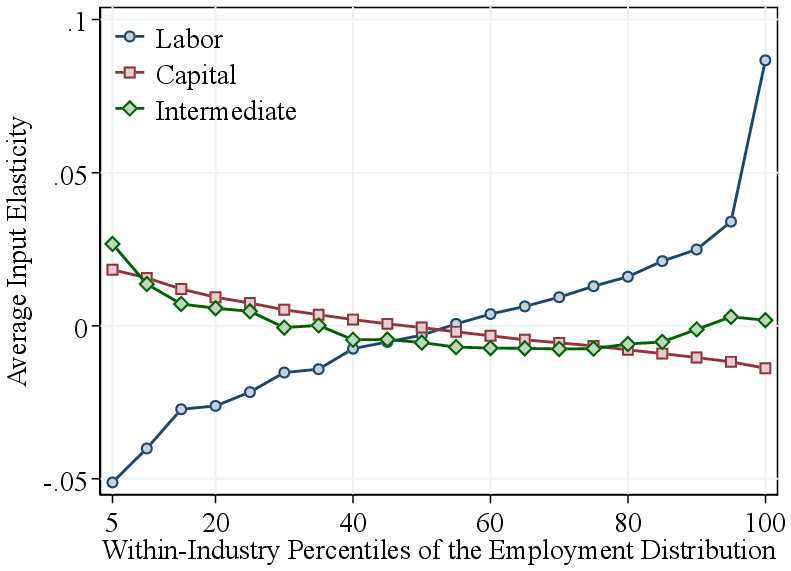

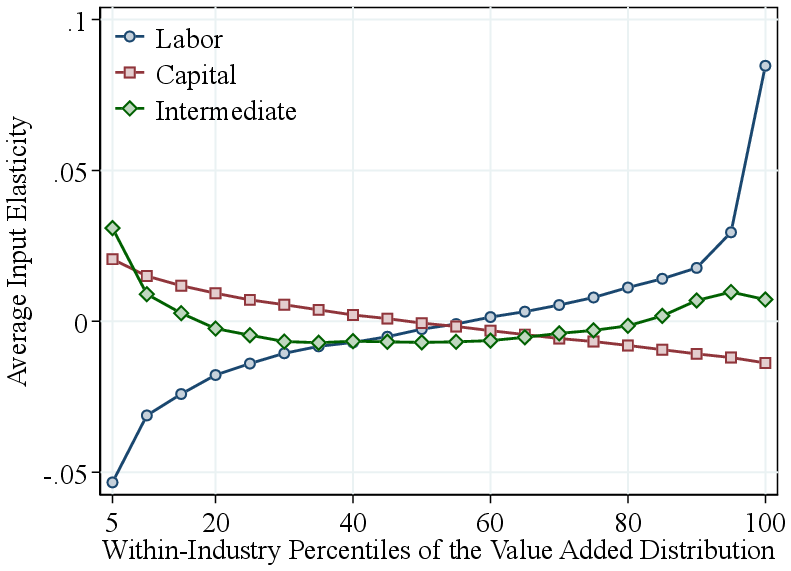

Appendix Figure A.5 presents the results when ranking firms, within industry, by employment or value added rather than by revenue. While the patterns for RTS are similar, the output elasticities display distinct variations: firms with high employment or high value added exhibit higher labor elasticities, whereas the intermediate input elasticity shows only a small increase among the largest firms. This pattern arises mechanically from the ranking criterion: firms with high employment or value added are, by construction, more labor-intensive. Therefore, we prefer to rank firms by revenue—a factor-neutral approach—in our primary analysis.

4.4 International Evidence

Our results are also robust across multiple samples and countries. We find similar patterns when analyzing U.S. manufacturing plants and firms in eleven European countries.

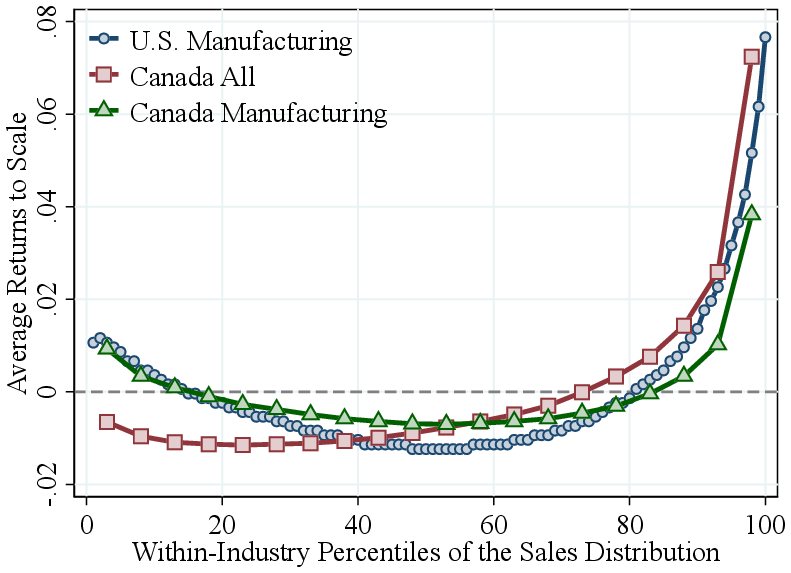

U.S. manufacturing. Our results are not unique to the Canadian economy but also hold for the U.S. manufacturing sector. Figure 6a shows the RTS–revenue relationship at the plant level, relative to the four-digit NAICS industry average. The pattern is U-shaped, with a notable steep increase at the top: RTS rises by about 9 p.p. from the 50th percentile to the top 1% of the revenue distribution. For comparison, we include a corresponding series for Canadian manufacturing in the same figure. Both sectors display similar U-shaped patterns, but the increase in RTS among the largest plants is more pronounced in the U.S., consistent with the longer right tail of the U.S. manufacturing size distribution (Leung et al., 2008).

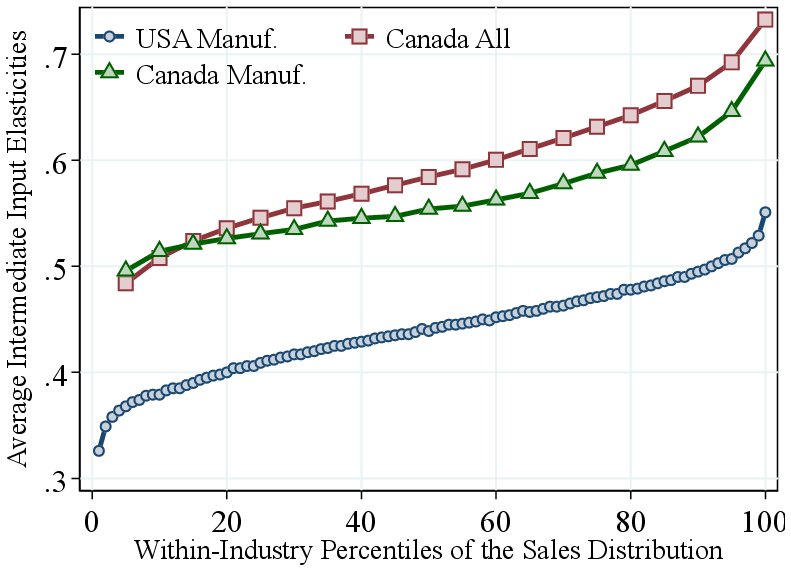

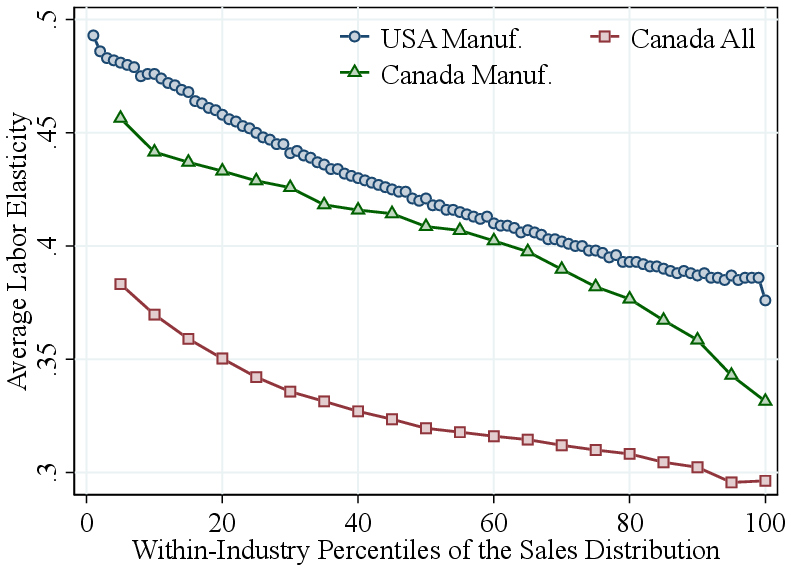

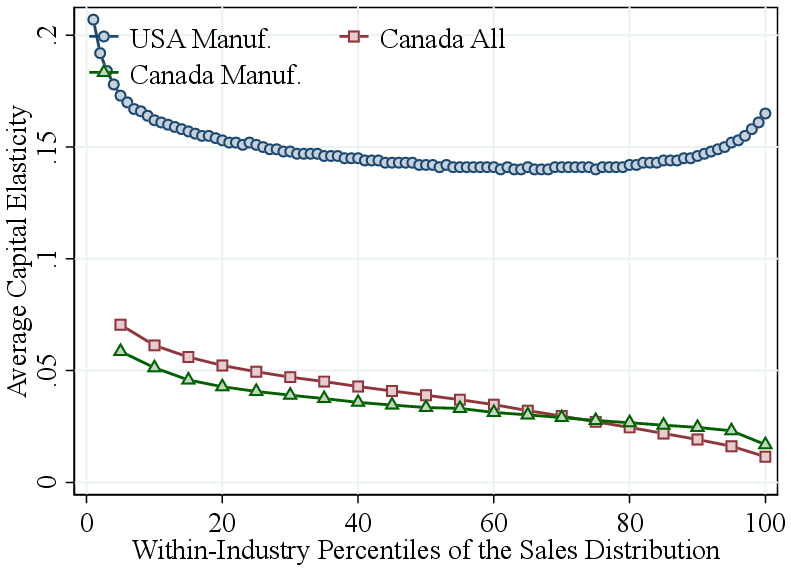

Remarkably, as in Canada, the increase in RTS is primarily driven by a rise in the output elasticity of intermediate inputs, which increases from about \(0.35\) at the bottom of the size distribution to around \(0.55\) for the largest U.S. plants (Figure A.4b). Furthermore, labor elasticities decline steadily with firm revenue, while capital elasticities decline up to the 90th percentile and then rise slightly among the very largest plants (Figure A.4). Revenue shares of labor, capital, and intermediate inputs across the revenue distribution also exhibit remarkably similar patterns between U.S. and Canadian manufacturing, and more broadly among all Canadian corporations (Figure A.6).

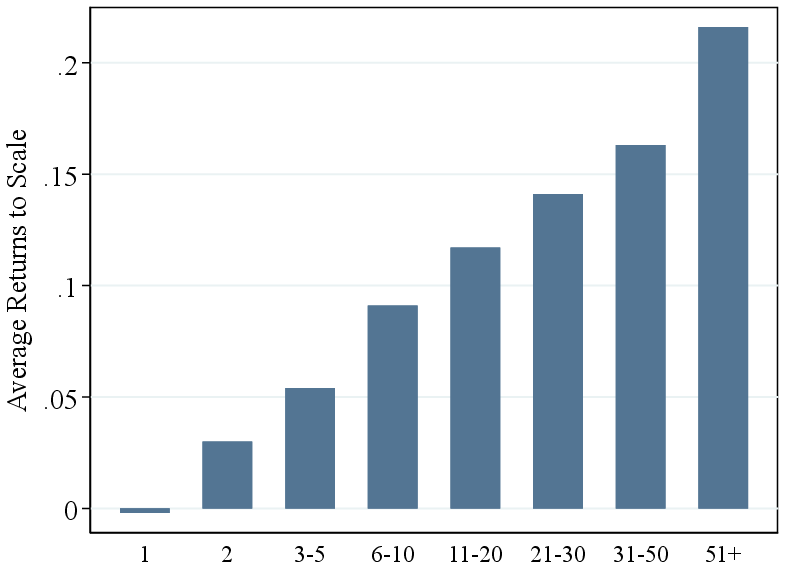

Our U.S. manufacturing production function estimates are at the plant level, whereas the Canadian data are measured at the firm level, which aggregates over multiple plants. In the Canadian data, we find that RTS increases significantly with the number of plants per firm (Figure A.9). However, controlling for the number of plants only slightly attenuates the RTS–revenue gradient: regressing demeaned RTS on log firm revenue yields a coefficient of \(0.012\), which drops modestly to \(0.010\) when controlling for plant count. Together with the U.S. manufacturing evidence, these results suggest that variation in RTS by firm revenue is not primarily driven by differences in the number of plants, but rather by systematic differences in production technologies across individual plants.

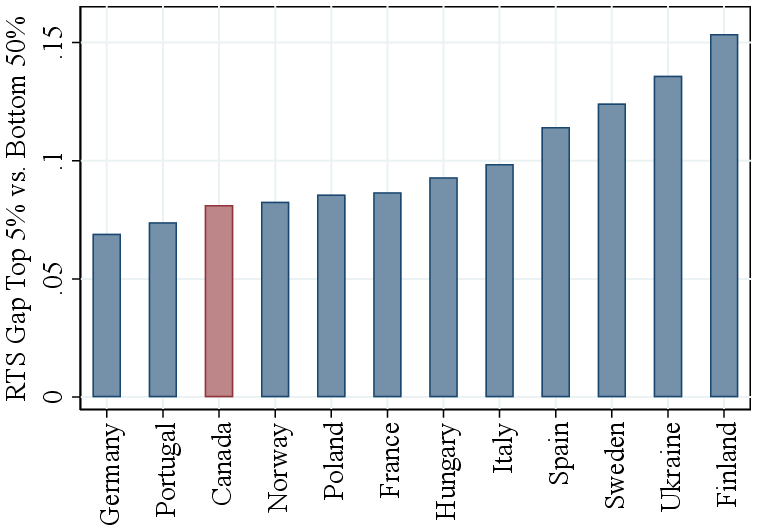

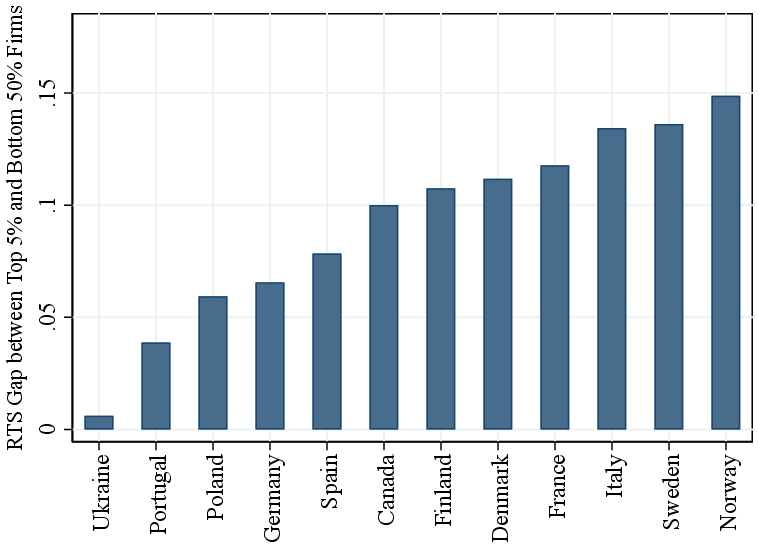

Notes: Figure 6a plots average RTS (demeaned by industry averages) against within-industry revenue percentiles for Canadian and U.S. manufacturing, as well as for the baseline economy-wide Canadian sample. Canadian results are shown within 5% quantiles of the revenue distribution. Figure 6b compares the within-industry RTS gap between the top 5% and bottom 50% of firms across 11 countries using Orbis data, including Canada for reference.

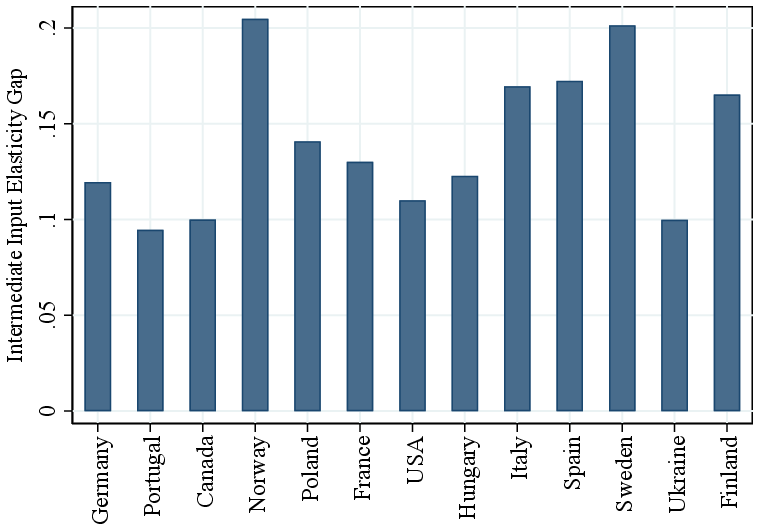

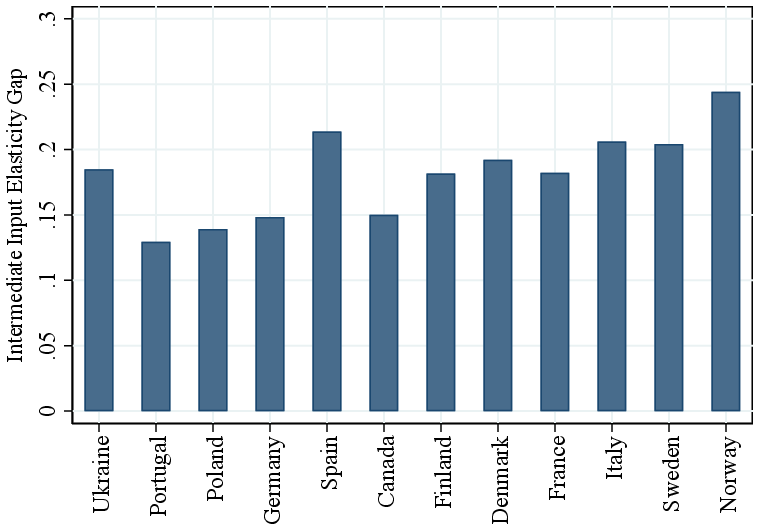

International evidence. Our results extend to several other countries using firm-level data from the Orbis database. Figure 6b shows estimates based on our baseline GNR method, applied within 2-digit NAICS industries across countries. We summarize the findings by plotting the average RTS difference between the top 5% and bottom 50% of the within-country-industry revenue distribution. The results are remarkably consistent across countries, with RTS differences ranging from about 7 p.p. in Germany to 15 p.p in Finland. Canada falls near the middle of this distribution, with similar patterns observed for other large European economies such as France and Italy. Consistent with our main results, we find that the intermediate input elasticity also increases strongly with firm size across countries (Figure A.1). Last, we apply the Demirer methodology to the Orbis data and find similar results (Figure A.2).

Implications for Firm Dynamics and Inequality. We now revisit several well-known empirical patterns in firm heterogeneity that have traditionally been attributed to TFP differences. For example, the literature has argued that firms with higher TFP grow faster (e.g., Sterk et al. (2021)), pay higher wages (e.g., Kline (2024)), and are disproportionately owned by wealthier households (e.g., Quadrini (2000); Cagetti and De Nardi (2006)). In this section, we argue that RTS differences are at least as important in explaining these empirical patterns.

4.4.1 Firm Dynamics

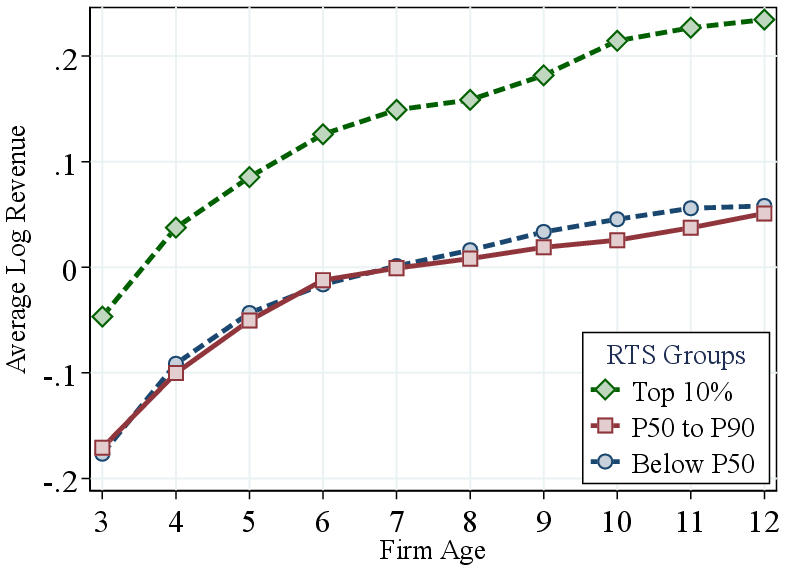

Heterogeneity in RTS has significant implications not only for the firm size distribution but also for firms’ growth trajectories over the life cycle. Firms with higher RTS are expected to grow faster to reach their larger optimal sizes, compared to firms with similar TFP but lower RTS. To analyze these life-cycle patterns, we construct a balanced panel of Canadian firms from our baseline estimates and group firms by their initial production function characteristics. Specifically, we focus on firms born between 2002 and 2005 that are observed for 12 consecutive years. We group firms based on their initial RTS and initial TFP, demeaned at the industry level. We then track their average log revenue, again demeaned within industries, over their life cycle (Figure 7).

(a) RTS (b) TFP

(b) TFP

Figure: Figure 7 – Life Cycle of Firms Starting with Different RTS and TFP

Notes: Figure 7 compares the life-cycle profile of revenue between firms with different initial RTS (Figure 8a) and TFP (Figure 8b). They are constructed using a balanced panel of firms which (i) are born between 2002 and 2005 and (ii) survive for at least 12 years. We demean firms’ initial RTS at the two-digit NAICS industry level. We bin firms into three groups based on their initial demeaned RTS in the left panel and three groups based on initial within-industry TFP percentiles in the right panel. Firm log revenue is also demeaned at the two-digit NAICS industry level.

Firms with higher initial RTS and TFP start with higher revenues relative to their industry peers. More importantly, firms with higher initial RTS (Panel A) exhibit significantly faster growth: firms in the top 10% of the initial RTS distribution grow about 30 log points over 10 years, whereas firms in the bottom 90% grow by only about 20 log points. This evidence supports our interpretation that high-RTS firms operate more scalable technologies, enabling substantially greater life-cycle growth. We also rank firms by their average growth rates over 12 years and find that the top 1% fastest-growing firms (“gazelles”) exhibit an average RTS of 0.98 compared to 0.95 among those below the 90th percentile. Similarly, Guntin and Kochen (2025) recently show that a firm dynamics model with ex-ante heterogeneity in production functions is required to explain empirical life cycle trajectories of the largest firms.

In contrast, Panel B shows that firms entering with high TFP, while initially larger, do not grow faster than other firms in their industry. Indeed, higher initial TFP is associated with slightly lower subsequent growth, which can be explained by TFP being a mean-reverting process. These finding suggest that highly productive firms might have low RTS, which constrains their growth (Hurst and Pugsley (2011)).

While these results focus on surviving firms, we also examine the effects of RTS and TFP heterogeneity on firm exit. We estimate probit regressions of firm exit on TFP percentile and RTS (Table A.15). Across specifications, higher RTS is associated with a lower probability of firm exit. The effect of TFP on firm exit is smaller, and varies in sign across specifications. We conclude that, from an ex ante perspective, RTS heterogeneity better predicts differences in firm growth and survival over the life cycle than TFP heterogeneity.

Finally, we investigate whether firms with varying RTS respond differently to aggregate shocks. We use two types of shocks: changes in industry-level TFP, and the 2007-2008 global financial crisis. We estimate regressions of firm revenue growth on RTS, the aggregate shock, and their interaction (Table A.16). The results show that firms with higher RTS respond more strongly to aggregate shocks, consistent with greater scalability (see also Smirnyagin (2023), Clymo and Rozsypal (2025), and Argente et al. (2024)).

4.4.2 Role of RTS Heterogeneity in Wealth and Wage Inequality

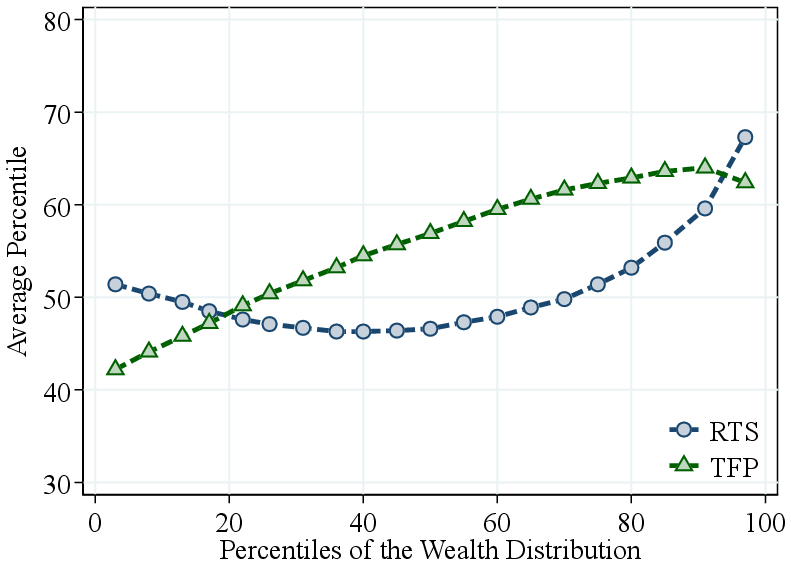

We conclude this section by examining how firm-level RTS relates to the wealth of firm owners and the wages of workers. First, we analyze how production function parameters vary with the equity wealth of business owners. A key advantage of our dataset is that we can link firms to their ultimate individual owners using administrative records from the Shareholder Information in Corporate Tax Files. We calculate each individual’s equity wealth by aggregating the value of the firms they own, weighted by ownership shares. For each owner, we then compute an equity-value-weighted average RTS and TFP percentile across the firms they own. Figure 8a shows that wealthier individuals tend to own firms with higher RTS. That is, owners at the top of the wealth distribution are more likely to own firms with more scalable production technologies. In addition, TFP is also increasing in owner wealth, but in a concave manner, particularly at the top of the distribution.

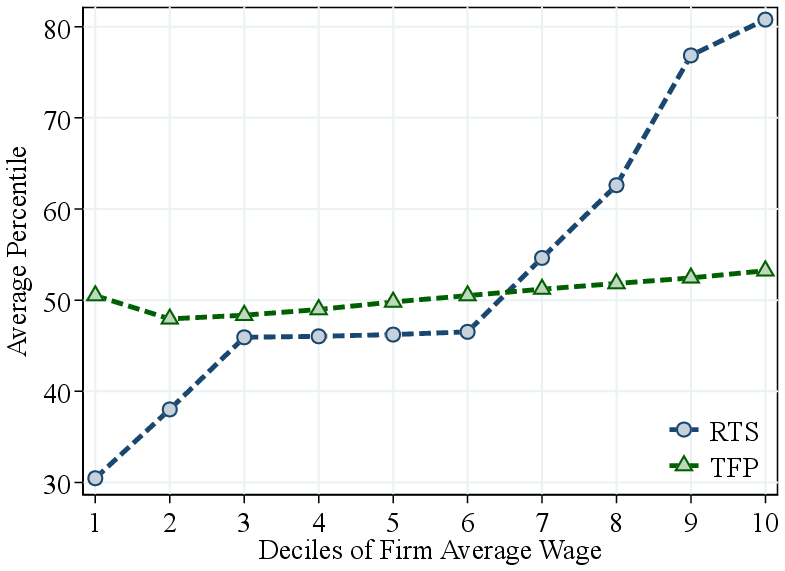

It is well established that large firms tend to pay higher wages than smaller firms for similar workers (Brown and Medoff (1989)). Given our results, a natural question is whether this firm size-wage premium is driven by higher TFP or greater scalability (RTS) among large firms. To disentangle these factors, we rank firms by their average wage and compute the average RTS and TFP across wage deciles. Figure 8b shows that higher-paying firms tend to have significantly higher RTS, while the relationship between wages and TFP is weaker and less systematic. These findings suggest that RTS heterogeneity is an important driver of the firm size-wage premium.

Notes: Figure 8a shows the average percentiles of RTS and TFP by percentiles of owners’ equity wealth. Figure 8b shows the average percentiles of RTS and TFP by deciles of firms’ average wage. Average wage is demeaned at the industry level. RTS and TFP percentiles are calculated within industry using our baseline (GNR) method.

5 Misallocation with RTS Heterogeneity

So far, we have documented substantial heterogeneity in RTS across firms and examined its implications for the firm size distribution. In this section, we study the theoretical and quantitative implications of this heterogeneity for a fundamental question in macroeconomics: the efficiency costs of financial frictions.

Our empirical results suggest that RTS heterogeneity is largely ex ante and persistent rather than driven by non-homotheticities. At the same time, our empirical approach measures RTS without tying it to a specific mechanism. Together, these findings motivate a model in which firms differ in an exogenous, highly persistent RTS type.

We employ an off-the-shelf quantitative model of entrepreneurship in the tradition of Quadrini (2000) and Cagetti and De Nardi (2006). Firms differ in both RTS (\(\eta\)) and TFP (\(z\)) in the (\(\eta,z\))-economy, while the benchmark \(z\)-economy features heterogeneity only in \(z\). By treating RTS symmetrically to TFP as an exogenous firm characteristic, comparing the two economies isolates how accounting for RTS heterogeneity changes the quantitative implications of financial frictions.

To exhibit the mechanism transparently, our baseline model is deliberately parsimonious. We show below that the main conclusions are robust in richer environments that more closely mirror the empirical setting. To build intuition, we first derive an analytical result in a static endowment economy and then quantify the mechanism in a dynamic setting.

5.1 Analytical Result in an Endowment Economy

We consider an endowment economy with aggregate input supply normalized to \(X=1\). A continuum of firms \(i\in [0,1]\), produces perfectly substitutable goods. A fraction \(\chi \in (0,1)\) of these firms face an input price wedge \(\tau \geq 0\), which distorts their input choices and constrains production. Each constrained firm is characterized by a pair of parameters \((\eta,z)\), where \(\eta \in (0,1)\) governs firm-level RTS and \(z\) is the firm’s TFP. Consistent with our empirical interpretation, we treat \(\eta\) as a given firm characteristic and interpret it as a summary statistic for scalability. The output of a constrained firm is given by \(y=f(x;z,\eta)=z\cdot x^{\eta}\). The remaining fraction of firms \(1-\chi\) is unconstrained and has constant returns to scale (\(\eta =1\)).20 The following proposition characterizes misallocation in terms of the output share and RTS of constrained firms:

Proposition 1. Consider an interior equilibrium where the output share of constrained firms is below one. Then, up to a second order approximation around the first best (\(\tau =0\)), the percent output loss associated with \(\tau\) is given by

\[\begin{align*} \Delta \ln Y \left (\tau \right) = \underbrace{\frac{\tau ^2}{2}}_\text{size of friction} \cdot \underbrace{\int _0^\chi w_i \cdot d i}_{\text{output share of constrained firms}} \cdot \underbrace{\int _0^\chi \frac{w_i}{\int _0^\chi w_j dj} \cdot \frac{\eta _i}{1-\eta _i} \cdot d i}_\text{avg. $\frac{RTS}{1-RTS}$ of constrained firms} \end{align*}\]

where \(w_i \equiv \frac{y_i^\star}{Y^\star}\) denotes the relative output of firm \(i\) in the first-best equilibrium.

Proof. See Appendix E.1 for the proof of the proposition. □

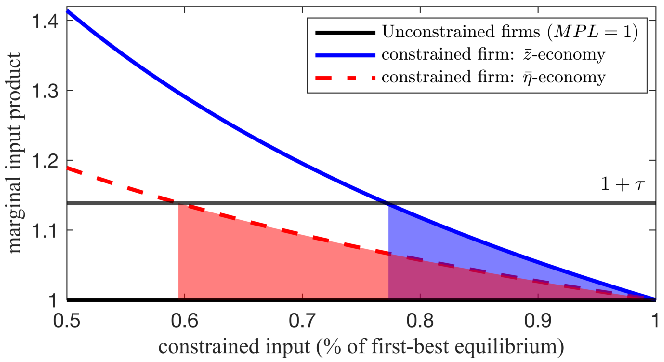

Notes: The figure provides a qualitative illustration of efficiency losses from input wedges for a representative constrained firm. In the \(\bar{{z}}\)-economy, the firm has high TFP (\(z=\bar{{z}},\eta =\eta _{0})\); in the \(\bar{{\eta}}\)-economy, the firm has high returns to scale (\(z=z_{0},\eta =\bar{\eta}\)), with \(0<z_{0}<\bar{z}\) and \(0<\eta _{0}<\bar{\eta}<1\). The shaded areas capture the implied output loss under each scenario.

The proposition shows that misallocation is proportional to the size of the friction and the output share of constrained firms. More importantly, it is increasing and convex in the (weighted-average) RTS of constrained firms (see also Atkeson et al. (1996) and Guner et al. (2008) for related points). Consequently, for a given wedge, misallocation is more severe when constrained firms have higher RTS. Furthermore, as a result of the convexity of misallocation in RTS, greater dispersion in RTS among constrained firms also leads to more severe misallocation.

Intuitively, a given input price wedge induces a larger quantity adjustment when RTS is high, as marginal products decline more slowly. This causes constrained firms to reduce their inputs more, leading to greater misallocation. In contrast, firm TFP affects misallocation only indirectly through its influence on the output share of constrained firms. We illustrate this in Figure 9, which compares the marginal input product of firms that would be “large” in the first-best allocation and contribute most to misallocation. The solid blue line represents the conventional setting where large firms have high TFP (\(\bar{{z}}\)), while the dashed red line represents an economy where large firms have high RTS (\(\bar{\eta}\)). For a given wedge \(\tau\), misallocation—represented by the area under the curve—is larger in the \(\bar{\eta}\)-economy.

5.2 Quantitative Dynamic Model

We now turn to the full dynamic model of entrepreneurship in the tradition of Quadrini (2000) and Cagetti and De Nardi (2006). Relative to the static environment, this model captures additional margins—capital accumulation, selection into entrepreneurship, and the endogenous composition of constrained firms—that shape the interaction between financial frictions and scalability. We quantify efficiency losses from financial frictions in the (\(\eta,z\))-economy and compare them to those in an otherwise identical \(z\)-economy.

5.2.1 Model Setup

Time is discrete and there is a unit continuum of agents who derive log utility from consumption. They discount the future at rate \(\tilde{{\beta}}\) and face a constant death probability \(p\in [0,1)\). Thus, their effective discount factor is \(\beta =(1-p)\cdot \tilde{{\beta}}\), and they maximize \(\mathbb{E}\left [\sum _{t\geq 0}\beta ^{t}\ln (c_{t})\right]\). Agents choose between employment and entrepreneurship, \(o\in \left \{W,E\right \}\). A worker earns labor income \(w\cdot h\), where \(w\) denotes the wage rate and \(h\) efficiency units of labor supply, which follow a first-order Markov process. Entrepreneurs are price takers in input and output markets, hire labor \(\ell\) and capital \(k\) at rental rates \(w\) and \(R\) to produce output \(z\cdot f(k,\ell)^{\eta}\), where \(f(\cdot)\) is a constant-returns-to-scale production function. The pair \((z,\eta)\) denotes entrepreneurial productivity \(z\) and project scalability \(\eta\), both treated as firm characteristics and assumed to follow a joint first-order Markov process. Consistent with our empirical findings, we model RTS as a persistent firm characteristic and abstract from non-homotheticities, which play a secondary role.

Asset markets are incomplete. Agents can invest their wealth \(a\geq 0\) in an annuity that pays an interest rate \(r\). Upon death, agents are replaced by an equal number of newborns who start with zero wealth. We parameterize financial frictions by \(\lambda \in [0,1]\), assuming that a fraction \(\lambda\) of total input expenditures must be financed with the entrepreneur’s own wealth. When this constraint binds, it generates a wedge between marginal products and input prices. As a result, static profit maximization yields a net profit of

\[\begin{align*} \pi (a,z,\eta) & =\max _{k\geq 0,\ell \geq 0}z\cdot f(k,\ell)^{\eta}-w\cdot \ell -R\cdot k\\ & \text{s.t.}w\cdot \ell +R\cdot k\leq \frac{a}{\lambda}, \end{align*}\]

implying input choices \(k(a,z,\eta),\ell (a,z,\eta)\) and output \(y(a,z,\eta)\).21 Thus, the agent’s dynamic problem can be written in recursive form as

\[\begin{align*} V(a,h,z,\eta) & =\max _{a'\geq 0,c\geq 0,o\in \left \{W,E\right \}}{u(c)}+\beta \cdot \mathbb{E}[V(a',h',z',\eta ')]\\ & \text{s.t}.\quad c+a'=\mathbb{{I}}_{o=W}\cdot w\cdot h+\mathbb{{I}}_{o=E}\cdot \pi (a,z,\eta)+(1+r)\cdot a. \end{align*}\]

We assume a competitive financial intermediary that invests in physical capital, subject to depreciation rate \(\delta\), and issues the annuities.

Equilibrium. We relegate the standard definition of equilibrium to Appendix E.2.

5.2.2 Calibration

We calibrate both the \((\eta,z)\)- and the \(z\)-economy to match the same set of observable moments of the firm size distribution and entrepreneurship dynamics. This isolates the role of RTS heterogeneity while holding fixed all other aspects of the environment. We follow a standard calibration strategy. First, we briefly discuss fixed common parameters. We set the death probability to \(\frac{1}{80}\), corresponding to an expected life expectancy of 80 years.22 We use a Cobb-Douglas production function \((f)\) with capital share \(\alpha =0.4\) and depreciation rate \(\delta =0.05\). Labor efficiency units \(h\) follow a log-normal AR(1) process with autocorrelation of \(0.9\) and cross-sectional standard deviation of \(1.3\), with mean normalized to \(\mu _{h}=-\frac{\sigma ^{2}_{h}}{2}\). We estimate this process directly from the data on individual post-tax earnings. We calibrate both economies at \(\lambda =0.3\), implying that 30% of input expenditures must be financed with the owner’s wealth, and then vary \(\lambda\) in counterfactuals.23

\((z)\)-Economy: We jointly calibrate five parameters \((\beta,\eta,\sigma _{z},\rho _{z},\xi _{z})\) to match six empirical moments as summarized in the middle column of Table II. The effective discount factor \(\beta\) primarily influences the aggregate capital-output ratio. The (common) RTS parameter \(\eta\) is closely tied to the fraction of the population engaged in entrepreneurship, as it governs the share of income accruing to entrepreneurs. Productivity \(z\) follows a log-normal AR(1) process with normalized mean \(\mu _{z}=-\frac{\sigma ^{2}_{z}}{2}\). Its persistence \((\rho _{z})\) shapes entry into and exit from entrepreneurship, while its cross-sectional dispersion, \(\sigma _{z}\), is central for matching the firm size distribution. To better capture the right tail, we model the top 1% of the \(z\)-distribution with a Pareto tail, where \(\xi _{z}\) governs tail thickness. Overall, the model matches the targeted moments closely.

| Data | Model | |||

| \(z\)-economy | \((\eta,z)\)-economy | |||

| A. Targeted moments | ||||

| Fraction entrepreneurs | 0.117 | 0.117 | 0.117 | |

| Transition rate W\(\rightarrow\)E | 0.021 | 0.021 | 0.021 | |

| Top 10% revenue share | 0.799 | 0.804 | 0.796 | |

| Top 1% revenue share | 0.522 | 0.515 | 0.524 | |

| Top 0.1% revenue share | 0.282 | 0.284 | 0.283 | |

| RTS: Top 5% vs bottom 50% (by revenue) | 0.083 | — | 0.083 | |

| Capital-output ratio | 2.970 | 2.970 | 2.971 | |

| B. Internally calibrated parameters | ||||

| Mean RTS | \(\mu _{\eta}\) | 0.683 | 0.782 | |

| Standard deviation RTS | \(\sigma _{\eta}\) | — | 0.054 | |

| Standard deviation log TFP | \(\sigma _{z}\) | 0.910 | 0.635 | |

| Persistence TFP | \(\rho _{z}\) | 0.970 | 0.954 | |

| Pareto tail TFP | \(\xi _{z}\) | 2.880 | — | |

| Correlation \((z,\eta)\) | \(\rho _{z,\eta}\) | — | -0.253 | |

| Discount factor | \(\beta\) | 0.902 | 0.890 | |

Notes: Steady-state calibration of the \((\eta,z)\) - and \(z\) -economy (both at \(\lambda =0.3\)). * not targeted. Data moments are derived from Canadian data, and the RTS gap corresponds to our baseline estimation.

\((\eta,z)\)-Economy: We extend the calibration of the \(z\)-economy by additionally disciplining heterogeneity in \(\eta\) to match the observed dispersion of RTS along the revenue distribution (rightmost column of Table II). Specifically, we model \(\eta\) as a truncated normal AR(1) process on the interval \((0,1)\) with parameters \((\mu _{\eta},\sigma _{\eta},\rho _{\eta})\). We set \(\rho _{\eta}=0.98\), matching the high persistence of RTS documented in the empirical analysis. The mean \(\mu _{\eta}\) helps determine the fraction of entrepreneurs, while the cross-sectional dispersion \(\sigma _{\eta}\) is closely linked to the difference in average RTS between the top 5% and the bottom 50% of firms ranked by revenue.24 We allow \(z\) and \(\eta\) to be correlated, but rather than imposing the empirically estimated joint distribution of \((\eta,z)\) directly, we calibrate the TFP process residually. This serves two purposes. First, it ensures that the \((\eta,z)\)-economy matches the same firm size distribution as the \(z\)-economy. Second, when firms operate production functions with different RTS, relative TFP levels are not directly comparable across firms, so the empirical joint distribution of \((\eta,z)\) cannot be taken at face value.25 Formally, we specify log TFP as \(\ln z=\sqrt{(1-\rho ^{2}_{z,\eta}}\tilde{{z}}+\rho _{z,\eta}\cdot \frac{\sigma _{z}}{\sigma _{\eta}}\cdot (\eta -\mu _{\eta})\), where \(\tilde{{z}}\) follows an independent normal AR(1) process with parameters \((\sigma _{z},\rho _{z},\mu _{z}=-\frac{\sigma ^{2}_{z}}{2})\). Under this parameterization, \(\sigma _{z}\) denotes the cross-sectional standard deviation of log TFP. Intuitively, both \(\rho _{z,\eta}\) and \(\sigma _{z}\) influence moments of the firm size distribution: when empirical RTS dispersion is small, the model requires greater residual TFP dispersion \(\sigma _{z}\) to match observed revenue concentration, while larger RTS dispersion implies a more negative correlation parameter \(\rho _{z,\eta}\).

In total, we calibrate six parameters to match seven empirical moments. This model version also matches the targeted moments closely and does not require a Pareto tail in \(z\) to replicate the right tail of the firm-size distribution; observed heterogeneity in RTS, combined with log-normal \(z\), is sufficient.

5.2.3 Quantitative Findings

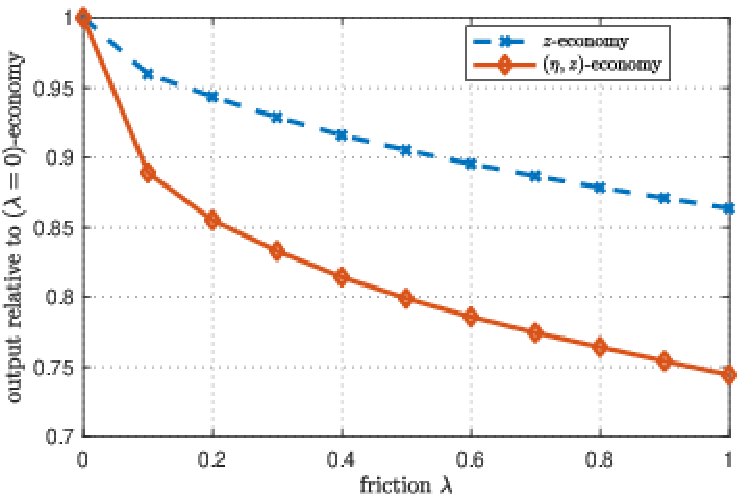

The two model economies are observationally equivalent in terms of the fraction of entrepreneurs, the persistence of entrepreneurship, the firm-size distribution, and the capital-output ratio. We evaluate the efficiency losses associated with the same financial friction in both economies. Figure 10 compares output losses as the financial friction parameter \(\lambda\) increases from the unconstrained case (\(\lambda =0\)) to \(\lambda =1\) across stationary equilibria. For \(\lambda =0.3\), corresponding to entrepreneurs financing 30 cents of each dollar of input expenditure with own wealth, the \((\eta,z)\)-economy—disciplined by empirical heterogeneity in both TFP and RTS—exhibits an output loss of 18.3 log points relative to the frictionless benchmark. By contrast, the conventional \(z\)-economy with homogeneous RTS incurs a significantly smaller loss of 7.4 log points. Thus, allowing for empirically measured RTS heterogeneity—while holding fixed the same observables and calibration targets—amplifies output losses from financial frictions by 147%.

Notes: The figure plots output as a function of the financial friction \(\lambda\), for both the \((z)\)- and the \((\eta,z)\)-economy. Output in both cases is normalized to one at \(\lambda =0\).

To understand this finding and connect it to the analytical mechanism in Section 5.1, we decompose the total log output loss into three terms: (i) static misallocation of production factors, holding fixed occupational choice; (ii) misallocation of talent across occupations; and (iii) under-accumulation of capital. Panel A of Table III shows that static misallocation of production factors across firms contributes 10.6 log points in the \((\eta,z)\)-economy—more than half of the total GDP loss and twice as much as in the conventional \(z\)-economy. This is precisely the channel highlighted in the analytical discussion: consistent with Proposition 1, a given input wedge distorts factor demand more for high-\(\eta\) firms. The dynamic setting further magnifies this effect through selection and accumulation: Consider two hypothetical superstar entrepreneurs that are initially poor and face the same financial friction. The one distinguished by high productivity (high \(z\)) can operate profitably even at small scale and therefore outgrows the constraint relatively quickly. In contrast, the one distinguished by high scalability (high \(\eta\)) is less profitable at small scale and consequently struggles to expand when constrained, leading to larger and more persistent misallocation.